Employers added 175,000 jobs last month, marking a hiring slowdown

U.S. unemployment rate rose slightly to 3.9% in April, continuing a stretch of remaining under 4% for 27 months.

Watch CBS News

U.S. unemployment rate rose slightly to 3.9% in April, continuing a stretch of remaining under 4% for 27 months.

The IRS is tapping Inflation Reduction Act funding to hire more agents and go after more tax cheats. Here's where it is focusing.

Audit firm BF Borgers allegedly failed to comply with accounting standards and fabricated audit documentation, regulators claim.

A Georgia senior living community fired an elderly worker shortly after honoring her as an employee of the year, regulators allege.

Job site Indeed identified the top 10 most sought-after job candidates by employers and recruiters. Here's what they found.

Peloton CEO Barry McCarthy exits as it lays off more staff. What's ailing the fitness company?

The recalled beef came from Cargill Meat Solutions in the form of burger patties and ground chuck.

Warren Buffett referred to close friend Charlie Munger as the "the architect of Berkshire Hathaway."

The retailer says the peelable treats have been "flying off the shelves" ever since TikTokers discovered the candy.

It may be a good idea to invest in gold this May. But, you should consider these pros and cons before you do.

There's a compelling case to be made for choosing a high-yield savings account over a CD this season.

Are you thinking about paying your mortgage off with your home equity? Here are pros and cons to consider first.

Tesla accounted for 80% of electric vehicle sales in the U.S. in 2020, but that figure fell to 55% last year.

The generative artificial intelligence boom has led to the emergence of romantic companion bots.

Apple said it will stop selling the devices later this month in order to comply with a U.S. import ban.

Alex Jones, the conspiracy theorist known for his fake news site InfoWars and his false denial of the Sandy Hook massacre, was permanently banned from Twitter in 2018.

More than 90 million consumers will scan a QR code this year. But the technology can also facilitate identity theft.

The billionaire owner of X took a defensive tone, saying that "the whole world will know that those advertisers killed the company."

OpenAI co-founder Sam Altman says he's looking forward to returning to the company, with the support of Microsoft's CEO, to build the 2 companies' "strong partnership."

Musk, who is under fire for supporting an antisemitic post, said the money will be donated to hospitals in Israel and to the Red Cross in Gaza.

Altman landed at Microsoft, the biggest investor in OpenAI, as former Twitch leader Emmett Shear was named OpenAI's new chief executive.

Minority Leader Hakeem Jeffries says Democrats are focused on getting work done while "extremists" within the Republican House majority are more interested in creating chaos.

The attack on Israel's Kerem Shalom prompted officials to close the terminal, disrupting critical shipments of food and other humanitarian aid into Gaza.

At least one child was killed and hundreds had to be rescued as portions of Texas dealt with flooding over the weekend.

South Dakota Gov. Kristi Noem has been under fire for details about killing her dog and a false claim about meeting with North Korea's leader in her new book.

KKR, one of the world's biggest private equity firms, has implemented employee ownership at dozens of companies, giving workers a stake in the businesses.

The Trump campaign told donors over the weekend that $76 million was raised in April between the RNC and the campaign, sources said.

Bernard Hill died Sunday at 79. The actor was known for his roles in "Lord of the Rings" and "Titanic."

Conservative groups look to peel off a key part of President Biden's base.

Two veteran astronauts will put the Starliner through its paces in the ship's first piloted flight to orbit.

With a relatively low average monthly cost of living and a low crime rate, this little-known town has a lot to offer retirees according to one report.

The U.S. is reaching "peak 65," marking the largest retirement wave in American history. But the financial outlook for many is grim.

Americans are underprepared for retirement, with the average account holding just $88,400 in savings.

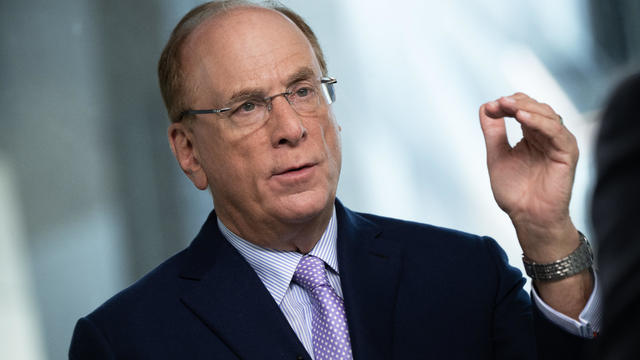

BlackRock CEO Larry Fink said that longer life expectancies are "putting the U.S. retirement system under immense strain."

About 1 in 8 workers think they'll retire by age 61. But the reality of saving for decades of expenses is daunting.

On this "Face the Nation" broadcast, Jordan's Queen Rania al Abdullah and South Dakota Gov. Kristi Noem join Margaret Brennan.

The Eta Aquariids meteor shower will peak overnight on Sunday into Monday, according to NASA.

South Dakota Gov. Kristi Noem has been under fire for details about killing her dog and a false claim about meeting with North Korea's leader in her new book.

At least one child was killed and hundreds had to be rescued as portions of Texas dealt with flooding over the weekend.

Two veteran astronauts will put the Starliner through its paces in the ship's first piloted flight to orbit.

Warren Buffett referred to close friend Charlie Munger as the "the architect of Berkshire Hathaway."

The retailer says the peelable treats have been "flying off the shelves" ever since TikTokers discovered the candy.

Audit firm BF Borgers allegedly failed to comply with accounting standards and fabricated audit documentation, regulators claim.

U.S. unemployment rate rose slightly to 3.9% in April, continuing a stretch of remaining under 4% for 27 months.

Job site Indeed identified the top 10 most sought-after job candidates by employers and recruiters. Here's what they found.

Conservative groups look to peel off a key part of President Biden's base.

The Trump campaign told donors over the weekend that $76 million was raised in April between the RNC and the campaign, sources said.

On this "Face the Nation" broadcast, Jordan's Queen Rania al Abdullah and South Dakota Gov. Kristi Noem join Margaret Brennan.

The following is a transcript of an interview with Rep. Ro Khanna, Democrat of California, that aired on May 5, 2024.

The following is a transcript of an interview with Sen. John Fetterman, Democrat of Pennsylvania, that aired on May 5, 2024.

The Texas dairy worker infected by H5N1 "did not disclose the name of their workplace," frustrating investigators.

Stress is hard to avoid, but experts say getting outdoors can have a positive impact on both our mental and physical health.

Actress Halle Berry joined with a group of bipartisan senators on Thursday to announce new legislation to promote menopause research, training and education.

New CDC data shows about 680 women in the U.S. died during pregnancy or shortly after childbirth in 2023, a decline from the previous year.

UnitedHealth Group CEO Andrew Witty disclosed that a cyberattack on one of its subsidiaries earlier this year might affect up to a third of all Americans.

Mexican officials say there's a high probability that three bodies found in a well are missing surfers from Australia and the U.S.

Madonna put on a free concert in Rio de Janeiro, turning a stretch of Copacabana beach into an enormous dance floor.

Massive floods in Brazil's southern Rio Grande do Sul state have killed at least 60 people and another 101 are reported missing, according to Sunday's toll from local authorities.

The attack on Israel's Kerem Shalom prompted officials to close the terminal, disrupting critical shipments of food and other humanitarian aid into Gaza.

The incident occurred in the parking lot of a hardware store in Willetton, a suburb in the west coast city of Perth, on Saturday night.

Bernard Hill died Sunday at 79. The actor was known for his roles in "Lord of the Rings" and "Titanic."

Madonna put on a free concert in Rio de Janeiro, turning a stretch of Copacabana beach into an enormous dance floor.

At 68 years old, and after about 100 films and 16 seasons on "The View," Whoopi Goldberg thinks there's still part of her you do not know. She talks about her new memoir, "Bits and Pieces: My Mother, My Brother, and Me."

At 68 years old, and after about 100 films and 16 seasons on "The View," Whoopi Goldberg thinks there's still part of her you do not know. She's penned a memoir, "Bits and Pieces: My Mother, My Brother, and Me," which she calls a "thank you" to her late mother, Emma, and late brother, Clyde. Goldberg talks with correspondent Seth Doane about her remarkable path, from a housing project in New York's Chelsea neighborhood, to a retreat overlooking a peninsula on the island of Sardinia.

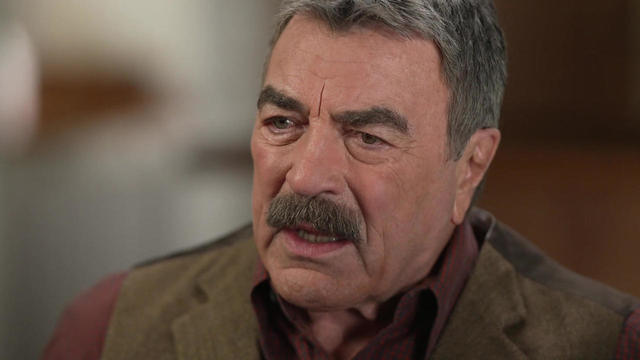

The hit CBS drama is set to end this year, but there's been pushback, most notably from its star. He talks about his desire to continue the show; his memoir, "You Never Know"; and the legacy of "Magnum, P.I."

Sidechat, an app launched in 2022 where students can post anonymously about their colleges, is becoming a tool for those choosing to protest at U.S. campuses. Amanda Silberling, a senior culture writer for TechCrunch, joins CBS News with more details on the app.

Microsoft users can now use biometric passkeys, like a thumbprint or Face ID, to sign into Microsoft 365, Copilot. Jon Fingas, senior editor at Techopedia, has more.

From labor shortages to environmental impacts, farmers are looking to AI to help revolutionize the agriculture industry. One California startup, Farm-ng, is tapping into the power of AI and robotics to perform a wide range of tasks, including seeding, weeding and harvesting.

Sidechat, an anonymous messaging app, has been used by students to share opinions and updates, but university administrators say it has also fueled hateful rhetoric.

Georgia is home to the nation's newest nuclear reactor. It's bringing clean energy to the state, but the project has run over budget and past its original completion date. Drew Kann, climate and environment reporter for The Atlanta Journal-Constitution, joins CBS News to explore the effort.

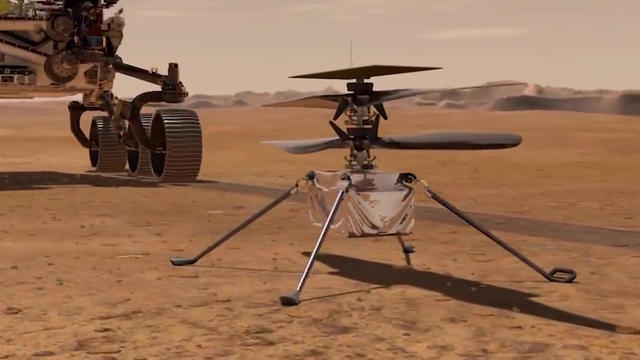

When NASA added a tiny four-pound helicopter as a stowaway to its Mars 2020 lander, it expected the helicopter to fly five very brief flights in the thin Martian atmosphere. Yet, Ingenuity would far surpass all expectations.

When NASA added a drone named Ingenuity to its Mars 2020 rover Perseverance, it expected the tiny four-pound helicopter to fly a total of five very brief missions in the thin Martian atmosphere. But Ingenuity far surpassed all expectations, flying dozens of flights before suffering damage to its rotors in January. Correspondent David Pogue reports on how the tiny drone, created from off-the-shelf parts, continued to provide valuable data and images from the Red Planet three years into its mission.

There's a newly-determined "major factor" in declining bumblebee populations – and it's attacking their nests.

On Monday, Boeing plans to launch astronauts on its new spacecraft that is called Starliner. The test flight to the International Space Station is years behind schedule.

Georgia is home to the nation's newest nuclear reactor. It's bringing clean energy to the state, but the project has run over budget and past its original completion date. Drew Kann, climate and environment reporter for The Atlanta Journal-Constitution, joins CBS News to explore the effort.

Mexican officials say there's a high probability that three bodies found in a well are missing surfers from Australia and the U.S.

Brian Fanion says he and his wife Amy Fanion had been arguing about his retirement plans when she picked up his service weapon and shot herself. Investigators did not believe his story.

Federal prosecutors said the men used fake badges, police lights and firearms to rob and kidnap Shamari Taylor for drug money.

Police in Wisconsin fatally shot a student who had pointed a pellet rifle in their direction outside a middle school, according to the state's Department of Justice.

In one find, a K-9 officer helped police find over a dozen fish buried in the sand and hidden behind logs and brush piles.

The Eta Aquariids meteor shower will peak overnight on Sunday into Monday, according to NASA.

Two veteran astronauts will put the Starliner through its paces in the ship's first piloted flight to orbit.

Boeing is expected to launch its Starliner space capsule that will take two astronauts to the International Space Station. CBS News consultant Bill Harwood breaks down Boeing's mission.

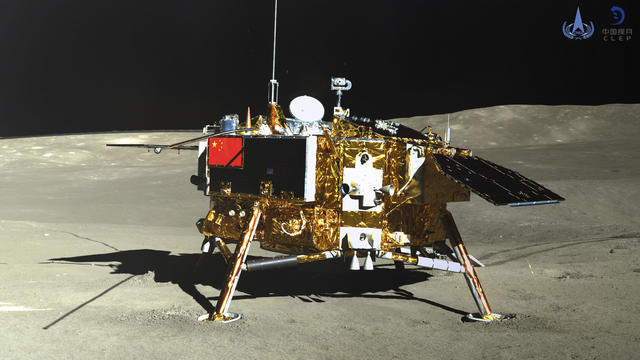

It is the latest advance in China's increasingly sophisticated space exploration program, which is now competing with the U.S.

Boeing is set to launch its first-ever spaceflight with humans next week. The Starliner spacecraft will lift off from Florida on Monday night for a multi-day mission to the International Space Station. Commander Barry "Butch" Wilmore and pilot Sunny Williams, two seasoned NASA astronauts who are a part of the mission, join CBS News to go over the flight.

A look back at the esteemed personalities who've left us this year, who'd touched us with their innovation, creativity and humanity.

The Francis Scott Key Bridge in Baltimore collapsed early Tuesday, March 26 after a column was struck by a container ship that reportedly lost power, sending vehicles and people into the Patapsco River.

When Tiffiney Crawford was found dead inside her van, authorities believed she might have taken her own life. But could she shoot herself twice in the head with her non-dominant hand?

We look back at the life and career of the longtime host of "Sunday Morning," and "one of the most enduring and most endearing" people in broadcasting.

Cayley Mandadi's mother and stepfather go to extreme lengths to prove her death was no accident.

David Korzyrkov fled Ukraine with his family two years ago when Russia invaded his country. Now, he's set to attend the Berklee College of Music in Boston. CBS Philadelphia's Josh Sanders has the story.

Hamas on Sunday attacked a border crossing with Israel as cease-fire talks appeared to be on the verge of collapse. Ramy Inocencio reports.

Boeing is preparing its Starliner capsule for its first piloted launch. The launch, scheduled for Monday, comes after years of delays and a ballooning budget. Mark Strassmann reports.

Democrats are rallying behind President Biden's response to pro-Palestinian protests, while Republicans pounced on Biden's position. Speculation is also increasing over who Trump will pick as his running mate. Skyler Henry reports.

Protests over the Israel-Hamas war continued on college campuses over the weekend, with some demonstrations spilling over into commencement ceremonies. Shanelle Kaul reports.