Federal Reserve holds rates steady. Here's the financial impact.

The Fed is leaving its benchmark interest rate unchanged, noting a lack of progress in curbing inflation.

Watch CBS News

The Fed is leaving its benchmark interest rate unchanged, noting a lack of progress in curbing inflation.

The Biden administration said it's erasing debt for people who attended the for-profit Art Institutes, which shut down in September.

Plaintiffs have three months to vote on whether to approve a proposed legal settlement that would resolve nearly all talc lawsuits.

"It's like trying to send a rocket to the moon in 1910 when the Wright Brothers were still working on their planes," one expert said.

Friends will soon be able to bet against each other on who will win Skee-Ball.

One ex-Tesla employee's post about the shock of losing his job amid a round of layoffs is sparking a workplace debate.

Trump's ownership stake in Trump Media & Technology group now stands at $5.7 billion, buoyed by a rise in the stock's price.

Witty said he himself made the decision that UnitedHealth would pay a ransom to the hackers who caused the massive data breach.

Inflation-weary consumers have also been slammed by high borrowing costs, but the Fed is cautious about sticky inflation.

Are you thinking about purchasing long-term care insurance at 65? Here's how much your coverage could cost.

If you're waiting for mortgage rates to drop, you could be in for a longer wait than anticipated. Here's why.

With high interest rates on hold, it may be time to consider a home equity loan. Here's why.

Tesla accounted for 80% of electric vehicle sales in the U.S. in 2020, but that figure fell to 55% last year.

The generative artificial intelligence boom has led to the emergence of romantic companion bots.

Apple said it will stop selling the devices later this month in order to comply with a U.S. import ban.

Alex Jones, the conspiracy theorist known for his fake news site InfoWars and his false denial of the Sandy Hook massacre, was permanently banned from Twitter in 2018.

More than 90 million consumers will scan a QR code this year. But the technology can also facilitate identity theft.

The billionaire owner of X took a defensive tone, saying that "the whole world will know that those advertisers killed the company."

OpenAI co-founder Sam Altman says he's looking forward to returning to the company, with the support of Microsoft's CEO, to build the 2 companies' "strong partnership."

Musk, who is under fire for supporting an antisemitic post, said the money will be donated to hospitals in Israel and to the Red Cross in Gaza.

Altman landed at Microsoft, the biggest investor in OpenAI, as former Twitch leader Emmett Shear was named OpenAI's new chief executive.

The Fed is keeping its benchmark interest rate in a range of 5.25% to 5.5%, the level it's held since July 2023.

Police ended protesters' occupation of a Columbia University building but violence erupted at UCLA and the University of Arizona as schools stepped up efforts to end demonstrations.

A similar repeal of Arizona's 1864 abortion ban passed the GOP-controlled House last week, and Gov. Katie Hobbs has said she'd sign the measure.

Columbia University called in the NYPD and cleared protesters from campus, ending a pro-Palestinian encampment on the school's main lawn.

Rep. Marjorie Tyalor Greene has dangled the threat of dethroning Johnson since late March after he relied on Democrats to push through a $1.2 trillion spending bill to avert a government shutdown.

An Oklahoma couple is in the ICU with broken backs and necks after a tornado tossed their truck into trees.

CBS News medical contributor Dr. Céline Gounder explains why experts hope more aggressive screening guidelines will help address some concerning breast cancer trends.

A famous white orca called "Frosty" was seen this week by a whale-watching tour group off the coast of Newport Beach in California.

The change doesn't mandate or even explicitly affirm LGBTQ clergy, but it means the church no longer forbids them.

With a relatively low average monthly cost of living and a low crime rate, this little-known town has a lot to offer retirees according to one report.

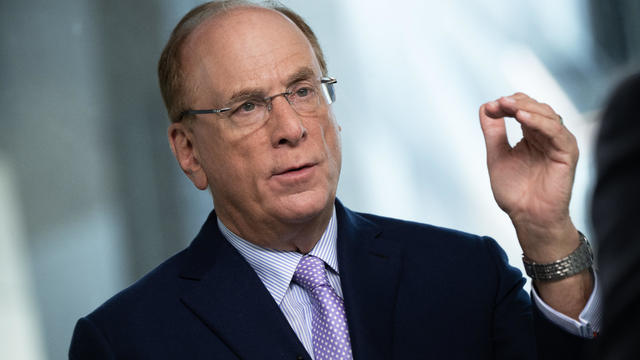

The U.S. is reaching "peak 65," marking the largest retirement wave in American history. But the financial outlook for many is grim.

Americans are underprepared for retirement, with the average account holding just $88,400 in savings.

BlackRock CEO Larry Fink said that longer life expectancies are "putting the U.S. retirement system under immense strain."

About 1 in 8 workers think they'll retire by age 61. But the reality of saving for decades of expenses is daunting.

The Fed is leaving its benchmark interest rate unchanged, noting a lack of progress in curbing inflation.

Plaintiffs have three months to vote on whether to approve a proposed legal settlement that would resolve nearly all talc lawsuits.

"It's like trying to send a rocket to the moon in 1910 when the Wright Brothers were still working on their planes," one expert said.

A similar repeal of Arizona's 1864 abortion ban passed the GOP-controlled House last week, and Gov. Katie Hobbs has said she'd sign the measure.

A famous white orca called "Frosty" was seen this week by a whale-watching tour group off the coast of Newport Beach in California.

The Fed is leaving its benchmark interest rate unchanged, noting a lack of progress in curbing inflation.

Plaintiffs have three months to vote on whether to approve a proposed legal settlement that would resolve nearly all talc lawsuits.

"It's like trying to send a rocket to the moon in 1910 when the Wright Brothers were still working on their planes," one expert said.

Witty said he himself made the decision that UnitedHealth would pay a ransom to the hackers who caused the massive data breach.

The Biden administration said it's erasing debt for people who attended the for-profit Art Institutes, which shut down in September.

A similar repeal of Arizona's 1864 abortion ban passed the GOP-controlled House last week, and Gov. Katie Hobbs has said she'd sign the measure.

The Biden administration said it's erasing debt for people who attended the for-profit Art Institutes, which shut down in September.

Rep. Marjorie Tyalor Greene has dangled the threat of dethroning Johnson since late March after he relied on Democrats to push through a $1.2 trillion spending bill to avert a government shutdown.

Democratic state Sen. Timothy Kennedy won a special election for the New York congressional seat left vacant by Democrat Brian Higgins' departure from Congress.

The FBI's searches, some of which were deemed to be improper in the past, were a flashpoint in a months-long fight in Congress over the reauthorization of Section 702 of FISA.

Plaintiffs have three months to vote on whether to approve a proposed legal settlement that would resolve nearly all talc lawsuits.

CBS News medical contributor Dr. Céline Gounder explains why experts hope more aggressive screening guidelines will help address some concerning breast cancer trends.

Recall involves shelled walnuts distributed in 19 states and sold in bulk bins at natural food and co-op stores.

Cat deaths and neurological disease are "widely reported" around farms where the H5N1 bird flu virus was detected, health officials say.

Methylene chloride, a toxic chemical, is linked to at least 88 deaths since 1980, federal regulators say.

Kenya's Red Cross says it helped rescue dozens of people from the Maasai Mara game park as deadly floods spreads across the region.

Blue holes are considered an "oasis" for marine life – but the Taam Ja' Blue Hole off the coast of Mexico remains largely mysterious.

Britain's government is claiming a "major milestone" in its controversial plan to fly anyone arriving in the U.K. without permission to Rwanda.

State media reported that a long section of a highway collapsed Wednesday in southern China, killing dozens.

In Israel for his 7th visit during the war in Gaza, Antony Blinken conveys "cautious optimism" to hostage families that a deal could be reached.

Judi Dench has tackled nearly every female role in William Shakespeare's plays, from Juliet to Cleopatra.

In her seven-decade career, Dame Judi Dench has played nearly every female character in William Shakespeare's plays, from Juliet to Cleopatra. Dench and her late husband even used to refer to Shakespeare as "the man who pays the rent." That's also the title of her new book, written with her friend Brendan O'Hea. First on "CBS Mornings", she shares stories from a lifetime of iconic Shakespearean roles and much more with Anthony Mason.

See who's nominated for the 77th annual Tony Awards. The Tonys will air live on CBS and Paramount+ on Sunday, June 16.

Only on CBS Mornings, Tony Award-winning actors Jesse Tyler Ferguson and Renée Elise Goldsberry announced the nominations in six key categories for the 77th Annual Tony Awards.

Britain's monarch, King Charles III, had put his official public duties on hold for weeks as he undergoes treatment for an unspecified cancer.

Pollen counters are turning to artificial intelligence as seasonal allergies worsen due to climate change. CBS News national correspondent Dave Malkoff explains how technology is changing the long and tedious process of pollen counting.

Artificial intelligence assistants may soon be able to do much more than play your favorite music or call your mom, but some Google researchers warn about possible ethical dilemmas. CBS News reporter Erica Brown has more.

From labor shortages to environmental impacts, farmers are looking to AI to help revolutionize the agriculture industry. One California startup, Farm-ng, is tapping into the power of AI and robotics to perform a wide range of tasks, including seeding, weeding and harvesting.

A newly-filed lawsuit targets two of the biggest generative AI platforms in the world, Open AI, the creators of ChatGPT and Microsoft's Copilot AI program.

If you think allergies are worse this year, you aren't imagining it. CBS News correspondent Dave Malkoff shows us how a hyperlocal pollen count could help people manage symptoms better.

Blue holes are considered an "oasis" for marine life – but the Taam Ja' Blue Hole off the coast of Mexico remains largely mysterious.

Pollen counters are turning to artificial intelligence as seasonal allergies worsen due to climate change. CBS News national correspondent Dave Malkoff explains how technology is changing the long and tedious process of pollen counting.

The bugs emit a loud, droning buzzing sound when they emerge — signaling they are ready to mate.

Officials from the National Weather Service and the CDC are already warning Americans about record-high temperatures in the coming months thanks to seasonal changes in the La Niña climate pattern. With these rising temperatures, there's also a higher risk of wildfires and droughts. Scott Dance, a climate reporter for The Washington Post, joined CBS News to discuss the forecast.

Bats have often been called scary and spooky but experts say they play an important role in our daily lives. CBS News' Danya Bacchus explains why the mammals are so vital to our ecosystem and the threats they're facing.

MS-13 members targeted random civilians so they could increase their status within the gang, prosecutors said.

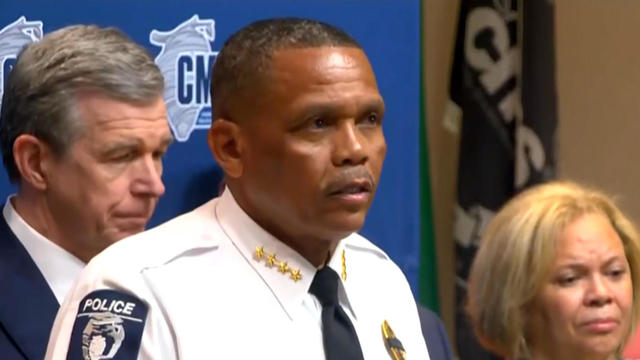

At least four law enforcement officers were killed during an operation in Charlotte, North Carolina, on Monday. Johnny Jennings, chief of the Charlotte-Mecklenburg Police Department, joins CBS News to discuss the case.

Four officers were killed Monday while trying to serve a warrant in Charlotte, North Carolina. The suspect, who was also killed, opened fire from the top floor of a house as the officers approached. Dave Malkoff has more on the slain officers.

Four law enforcement officers were killed and another four injured during a U.S. Marshals Service fugitive task force operation in Charlotte, North Carolina, Monday. A suspect was killed during the standoff, according to the Charlotte-Mecklenburg police chief. CBS News' Manuel Bojorquez has the latest confirmed information.

Authorities say they may have stopped a serial killer from striking again, after a man confessed to murdering two women.

The Horsehead Nebula, which NASA has called "one of the most distinctive objects in our skies," is located in the constellation Orion.

Astronauts Barry Wilmore and Sunita Williams say they have complete confidence in the Starliner despite questions about Boeing's safety culture.

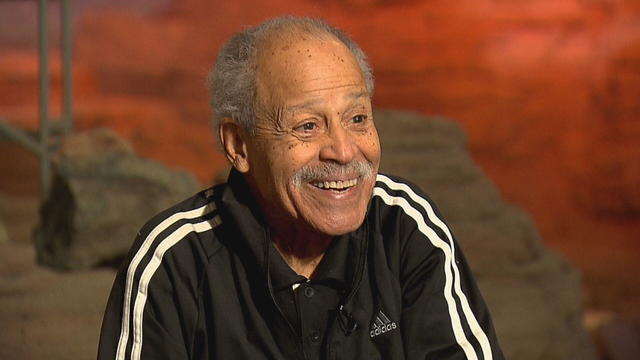

In 1961, Ed Dwight was selected by President John F. Kennedy to enter an Air Force training program known as the path to NASA's Astronaut Corps. But he ultimately never made it to space.

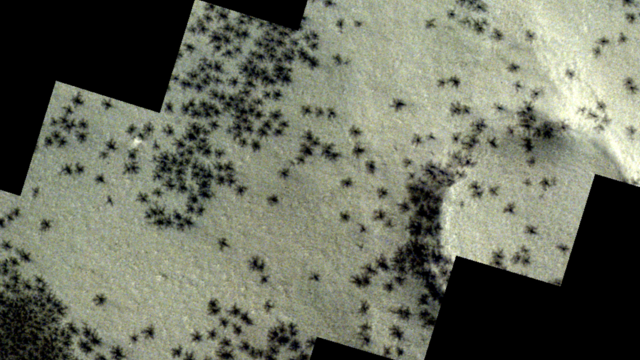

The creepy patterns were observed by the European Space Agency's ExoMars Trace Gas Orbiter.

The Shenzhou 18 crew will replace three taikonauts aboard the Chinese space station who are wrapping up a six-month stay.

A look back at the esteemed personalities who've left us this year, who'd touched us with their innovation, creativity and humanity.

The Francis Scott Key Bridge in Baltimore collapsed early Tuesday, March 26 after a column was struck by a container ship that reportedly lost power, sending vehicles and people into the Patapsco River.

When Tiffiney Crawford was found dead inside her van, authorities believed she might have taken her own life. But could she shoot herself twice in the head with her non-dominant hand?

We look back at the life and career of the longtime host of "Sunday Morning," and "one of the most enduring and most endearing" people in broadcasting.

Cayley Mandadi's mother and stepfather go to extreme lengths to prove her death was no accident.

The Federal Reserve will keep its benchmark rate steady, a sign that inflation has not yet come down to the targeted rate. CBS News' Jill Schlesinger and Jo Ling Kent look ahead to what this means for Americans.

The Federal Reserve is not expected to cut interest rates Wednesday as inflation persists. CBS News contributor J.D. Durkin breaks down the data.

The U.S. Preventative Services Task Force is now recommending women get a mammogram every other year beginning at age 40, a significant update from the previous recommendation of screenings starting at 50. Dr. John Wong, vice chair of the U.S. Preventative Services Task Force, joins CBS News to discuss the change.

A new article by The Wall Street Journal says "hey" is now the most dreaded word at work, causing stress with its open-ended connotations. Dr. Bryan Robinson, psychotherapist and author of the book, "Chained to the Desk in a Hybrid World: A Guide to Work-Life Balance," joins CBS News to discuss the impact of the word.

Police on Wednesday removed an encampment of pro-Palestinian protesters at the University of Wisconsin-Madison. Officials there said at least a dozen arrests were made and police would remain on the scene, but that they aren't asking protesters to leave.