Donald Trump is about to become $1.3 billion richer. Here's why.

Former President Donald Trump could receive a large windfall from his newly public media company, Trump Media & Technology Group.

Watch CBS News

Former President Donald Trump could receive a large windfall from his newly public media company, Trump Media & Technology Group.

UnitedHealth said it paid the criminals behind attack that crippled hospitals and pharmacies to protect sensitive patient data.

A "concierge service" that lets paying members bypass airport security lines is unfair to other travelers, California lawmaker says.

A bill that could ultimately ban TikTok in the U.S. will soon head for a vote in the Senate. Here's what experts say to expect next.

Millions of Americans filed their taxes during the last two weeks of this year's tax season. Here's how to find out when you'll get your refund.

Customers who rely on government assistance programs can get same perks as Prime members, for less.

Proposed deal "threatens to deprive consumers of the competition for affordable handbags," federal agency says.

Cancer, heart disease, respiratory illnesses and kidney dysfunction among the health consequences of a warming planet.

Tesla reduced prices by $2,000 on three of its five models in the U.S. and also slashed prices in China and Germany.

If you're looking for ways to resolve your overwhelming credit card debt, these strategies are worth considering.

Long-term care insurance doesn't just cover nursing homes. Here are six other things it can cover.

Are you a senior dealing with the high costs of inflation? Then consider making these three smart moves now.

Tesla accounted for 80% of electric vehicle sales in the U.S. in 2020, but that figure fell to 55% last year.

The generative artificial intelligence boom has led to the emergence of romantic companion bots.

Apple said it will stop selling the devices later this month in order to comply with a U.S. import ban.

Alex Jones, the conspiracy theorist known for his fake news site InfoWars and his false denial of the Sandy Hook massacre, was permanently banned from Twitter in 2018.

More than 90 million consumers will scan a QR code this year. But the technology can also facilitate identity theft.

The billionaire owner of X took a defensive tone, saying that "the whole world will know that those advertisers killed the company."

OpenAI co-founder Sam Altman says he's looking forward to returning to the company, with the support of Microsoft's CEO, to build the 2 companies' "strong partnership."

Musk, who is under fire for supporting an antisemitic post, said the money will be donated to hospitals in Israel and to the Red Cross in Gaza.

Altman landed at Microsoft, the biggest investor in OpenAI, as former Twitch leader Emmett Shear was named OpenAI's new chief executive.

Follow live updates as former President Donald Trump's criminal trial resumes in New York.

Antisemitic chants and even threats against Jewish students have brought the tension of the Middle East onto U.S. college campuses.

Scammers have been increasingly successful in leveraging their romantic grip on victims by turning them into unwitting co-conspirators, or "money mules."

Former President Donald Trump could receive a large windfall from his newly public media company, Trump Media & Technology Group.

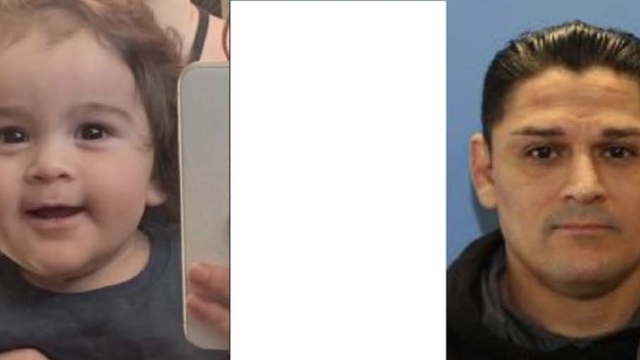

Authorities in Washington state are searching for a former officer accused of killing two women and abducting a child.

The Senate is expected to approve the foreign aid package this week after months of disagreement in Congress.

A Minnesota state senator now faces charges in connection to a burglary at a Detroit Lakes home earlier this week.

A new U.K. law means asylum seekers arriving on British shores without prior permission can be deported to East Africa.

The photo of Prince Louis is said to have been taken by his mother Catherine, Princess of Wales.

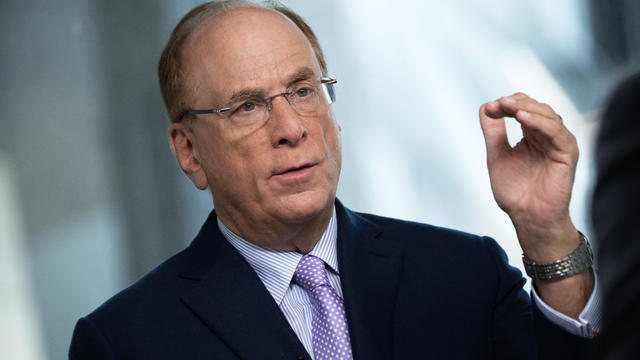

The U.S. is reaching "peak 65," marking the largest retirement wave in American history. But the financial outlook for many is grim.

Americans are underprepared for retirement, with the average account holding just $88,400 in savings.

BlackRock CEO Larry Fink said that longer life expectancies are "putting the U.S. retirement system under immense strain."

About 1 in 8 workers think they'll retire by age 61. But the reality of saving for decades of expenses is daunting.

America's retirement system has left behind 90% of workers. "We see big gaps with the rich and the poor in terms of who gets to retire," one expert said.

About 100 victims of Larry Nassar, who was convicted of sexual abuse and child pornography, will receive a settlement from the Justice Department.

Trump made 10 social media posts that were "threatening, inflammatory," prosecutors said, arguing he should pay a fine for each post.

Customers who rely on government assistance programs can get same perks as Prime members, for less.

Authorities in Washington state are searching for a former officer accused of killing two women and abducting a child.

In November 2023, NASA's Voyager 1 spacecraft stopped sending "readable science and engineering data."

Customers who rely on government assistance programs can get same perks as Prime members, for less.

UnitedHealth said it paid the criminals behind attack that crippled hospitals and pharmacies to protect sensitive patient data.

Former President Donald Trump could receive a large windfall from his newly public media company, Trump Media & Technology Group.

Proposed deal "threatens to deprive consumers of the competition for affordable handbags," federal agency says.

A bill that could ultimately ban TikTok in the U.S. will soon head for a vote in the Senate. Here's what experts say to expect next.

Trump made 10 social media posts that were "threatening, inflammatory," prosecutors said, arguing he should pay a fine for each post.

The Senate is expected to approve the foreign aid package this week after months of disagreement in Congress.

Follow live updates as former President Donald Trump's criminal trial resumes in New York.

As of the end of March, more than 187,000 Ukrainians have arrived in the U.S. under the Uniting for Ukraine program, resettling with resounding efficiency and relatively little controversy.

The NYPD made several arrests at a pro-Palestinian protest outside NYU's Stern School of Business in Gould Plaza.

UnitedHealth said it paid the criminals behind attack that crippled hospitals and pharmacies to protect sensitive patient data.

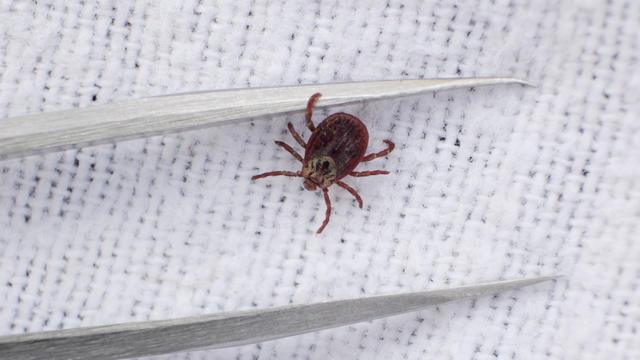

Warmer weather is prime time for ticks that can carry Lyme disease and other illnesses. Here's how to spot them and get rid of them.

Tires emit huge volumes of particles and chemicals as they roll along the highway, and researchers are only beginning to understand the threat. One byproduct of tire use, 6PPD-q, is in regulators' crosshairs after it was found to be killing fish.

Cancer, heart disease, respiratory illnesses and kidney dysfunction among the health consequences of a warming planet.

To reduce recidivism, some rural counties are hiring community health workers or peer support specialists to connect people leaving custody to mental health, substance use treatment, medical services and jobs.

The photo of Prince Louis is said to have been taken by his mother Catherine, Princess of Wales.

The wreck is "partly disintegrated," but some remnants have been "very well preserved."

A new U.K. law means asylum seekers arriving on British shores without prior permission can be deported to East Africa.

In his final letter before he vanished on Mount Everest, George Mallory said his chances of reaching the world's highest peak were "50 to 1 against us."

As of the end of March, more than 187,000 Ukrainians have arrived in the U.S. under the Uniting for Ukraine program, resettling with resounding efficiency and relatively little controversy.

Emmy and Tony Award-winning actress Bebe Neuwirth is back on Broadway, starring as Fraulein Schneider in the new revival of "Cabaret."

Chanel Miller, celebrated for her profound memoir "Know My Name," steps into a new creative realm with her children's book, "Magnolia Wu Unfolds It All." The story, both written and illustrated by Miller, follows two young friends on an adventurous quest through New York City to return misplaced socks from Magnolia's parents' laundromat.

Country music star Eric Church has had a standout year, marked by the opening of his new bar, restaurant and venue called “Chief's” in Nashville. In addition to launching this highly-anticipated spot, Church is playing a 19-show residency there.

First on "CBS Mornings," we're getting a first listen to a never-before-heard song from Aaron Carter. Carter died in 2022 after struggling with addiction and mental health issues. Now, his team and his sister, Angel Carter Conrad, are releasing his previously unheard music. "The Recovery Album" comes out May 24. Part of the proceeds will go to the nonprofit "The Kids Mental Health Foundation," formerly known as "On Our Sleeves."

Facing widespread unhappiness over its response to the Israel-Hamas war, the writers' group PEN America has called off its annual awards ceremony.

Customers who rely on government assistance programs can get same perks as Prime members, for less.

Secretary of Commerce Gina Raimondo is at the center of a global competition for semiconductor dominance. It's a battle that also puts her at the center of two of the hottest global national security hotspots. Lesley Stahl of 60 Minutes spoke with Raimondo for the broadcast.

From labor shortages to environmental impacts, farmers are looking to AI to help revolutionize the agriculture industry. One California startup, Farm-ng, is tapping into the power of AI and robotics to perform a wide range of tasks, including seeding, weeding and harvesting.

A bill that could ultimately ban TikTok in the U.S. will soon head for a vote in the Senate. Here's what experts say to expect next.

More than 100 nations, including the United States, have agreed to protect 30% of the world's oceans by 2030.

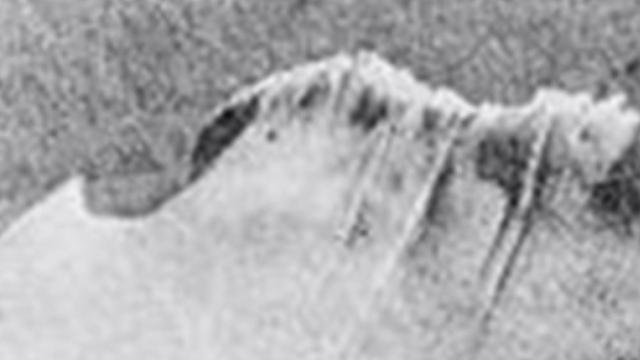

A photo taken two days after the sinking of the RMS Titanic apparently shows the iceberg that doomed the so-called unsinkable ship in 1912. CBS News' John Dickerson has details.

Despite how terrifying sharks might seem, the creatures are critical to the survival of the world's oceans. Oceans generate 50% of the oxygen on the planet and absorb 90% of excess heat created by global warming. CBS News senior national and environmental correspondent Ben Tracy spoke with conservationists in the Bahamas.

A new CBS poll finds that most of the public favors the U.S. taking steps to address climate change. CBS News executive director of elections and surveys Anthony Salvanto breaks down the numbers.

Climate change could cause a $38 trillion income loss per year globally by 2049, according to a new study by the Potsdam Institute for Climate Impact Research. CBS News' Lilia Luciano breaks down the numbers.

A recent report by the United Nations warned that 1 million species are at risk of extinction because of climate-related issues, and some scientists say the number could be even higher. CBS News national environmental correspondent David Schechter has more.

About 100 victims of Larry Nassar, who was convicted of sexual abuse and child pornography, will receive a settlement from the Justice Department.

Authorities in Washington state are searching for a former officer accused of killing two women and abducting a child.

A Minnesota state senator now faces charges in connection to a burglary at a Detroit Lakes home earlier this week.

Scammers have been increasingly successful in leveraging their romantic grip on victims by turning them into unwitting co-conspirators, or "money mules."

Prosecutors objected some of the survey questions about Bryan Kohberger and the deaths of four University of Idaho students.

In November 2023, NASA's Voyager 1 spacecraft stopped sending "readable science and engineering data."

In two weeks, Boeing's Starliner spacecraft is scheduled to launch its first piloted test flight, bringing two veteran NASA astronauts to the International Space Station. Astronaut Matt Dominick joined CBS News from the ISS to talk about the mission and life in space.

A process called cryopreservation allows cells to remain frozen but alive for hundreds of years. For some animal cells, the moon is the closest place that's cold enough.

The Lyrid meteor show is set to peak as the week begins.

April's full moon, known as the Pink Moon, will reach peak illumination on Tuesday, but it will appear full from Monday morning through Thursday morning.

A look back at the esteemed personalities who've left us this year, who'd touched us with their innovation, creativity and humanity.

The Francis Scott Key Bridge in Baltimore collapsed early Tuesday, March 26 after a column was struck by a container ship that reportedly lost power, sending vehicles and people into the Patapsco River.

When Tiffiney Crawford was found dead inside her van, authorities believed she might have taken her own life. But could she shoot herself twice in the head with her non-dominant hand?

We look back at the life and career of the longtime host of "Sunday Morning," and "one of the most enduring and most endearing" people in broadcasting.

Cayley Mandadi's mother and stepfather go to extreme lengths to prove her death was no accident.

A 10-foot-long alligator was wrangled and relocated after wandering onto the tarmac at MacDill Air Force Base near Tampa, Florida.

Donald Trump's Tuesday began with a contempt hearing over whether the former president violated a gag order in his ongoing "hush money" trial in New York. CBS News national correspondent Errol Barnett and CBS News legal contributor Jessica Levinson have more on the hearing and the rest of the case.

A Brazilian woman brought a 68-year-old man in a wheelchair into a bank branch and tried to get him to sign for a loan, police said. Bank staff became suspicious and called the police, who said he had been dead for hours. Local media reported that the family's lawyer disputed the account offered by police, saying "the facts did not happen as stated" and that the man had arrived at the bank alive.

A surfing accident left New York teacher Billy Keenan paralyzed, but when he received a call from a police officer, his life changed.

In two weeks, Boeing's Starliner spacecraft is scheduled to launch its first piloted test flight, bringing two veteran NASA astronauts to the International Space Station. Astronaut Matt Dominick joined CBS News from the ISS to talk about the mission and life in space.