Donald Trump is $1.8 billion richer after getting DJT stock bonus

Trump's ownership stake in Trump Media & Technology group now stands at $5.7 billion, buoyed by a rise in the stock's price.

Watch CBS News

Trump's ownership stake in Trump Media & Technology group now stands at $5.7 billion, buoyed by a rise in the stock's price.

One ex-Tesla employee's post about the shock of losing his job amid a round of layoffs is sparking a workplace debate.

Friends will soon be able to bet against each other on who will win Skee-Ball.

Methylene chloride, a toxic chemical, is linked to at least 88 deaths since 1980, federal regulators say.

Reports of elder fraud crimes increased by 14% in 2023, according to a new federal report.

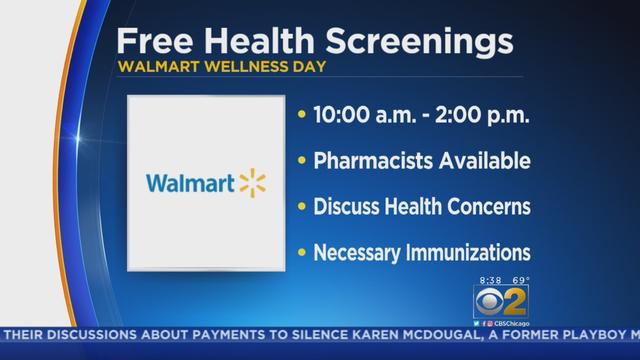

In an abrupt switch, Walmart plans to shut 51 health clinics in six states and pull the plug on telemedicine services.

Wyoming and North Dakota had the highest rate of employee fatalities, according to an analysis from labor union AFL-CIO

Walmart said its new store brand Bettergoods is "chef-inspired," and offers dozens of upscale products like plant-based milks.

Recall involves shelled walnuts distributed in 19 states and sold in bulk bins at natural food and co-op stores.

Debt relief may not help with all types of debt. Find out what types of debt most debt relief services help with.

With the latest Federal Reserve meeting underway, there's a compelling case to be made for opening a long-term CD now.

Borrowing from your home equity can be a smart option to consider, but there are some risks to be aware of, too.

Tesla accounted for 80% of electric vehicle sales in the U.S. in 2020, but that figure fell to 55% last year.

The generative artificial intelligence boom has led to the emergence of romantic companion bots.

Apple said it will stop selling the devices later this month in order to comply with a U.S. import ban.

Alex Jones, the conspiracy theorist known for his fake news site InfoWars and his false denial of the Sandy Hook massacre, was permanently banned from Twitter in 2018.

More than 90 million consumers will scan a QR code this year. But the technology can also facilitate identity theft.

The billionaire owner of X took a defensive tone, saying that "the whole world will know that those advertisers killed the company."

OpenAI co-founder Sam Altman says he's looking forward to returning to the company, with the support of Microsoft's CEO, to build the 2 companies' "strong partnership."

Musk, who is under fire for supporting an antisemitic post, said the money will be donated to hospitals in Israel and to the Red Cross in Gaza.

Altman landed at Microsoft, the biggest investor in OpenAI, as former Twitch leader Emmett Shear was named OpenAI's new chief executive.

After the school declared a pro-Palestinian encampment unlawful, a clash between dozens of protesters and counter-protesters led to one person being driven away in an ambulance.

Dozens of people were arrested. The school asked police to move in less than 24 hours after the pro-Palestinian demonstrators took over the building.

Prosecutors in former President Donald Trump's criminal trial in New York called their fifth witness to the stand as proceedings continued Tuesday.

The Biden administration is considering bringing certain Palestinians fleeing war-torn Gaza to the U.S. as refugees, according to internal federal government documents obtained by CBS News.

The proposal would recognize the medical uses of cannabis and acknowledge it has less potential for abuse than some other drugs.

Trump's ownership stake in Trump Media & Technology group now stands at $5.7 billion, buoyed by a rise in the stock's price.

Methylene chloride, a toxic chemical, is linked to at least 88 deaths since 1980, federal regulators say.

Tuesday's storms came just two days after tornadoes tore through Oklahoma on Sunday, killing four people and injuring at least 100.

The FBI's searches, some of which were deemed to be improper in the past, were a flashpoint in a months-long fight in Congress over the reauthorization of Section 702 of FISA.

With a relatively low average monthly cost of living and a low crime rate, this little-known town has a lot to offer retirees according to one report.

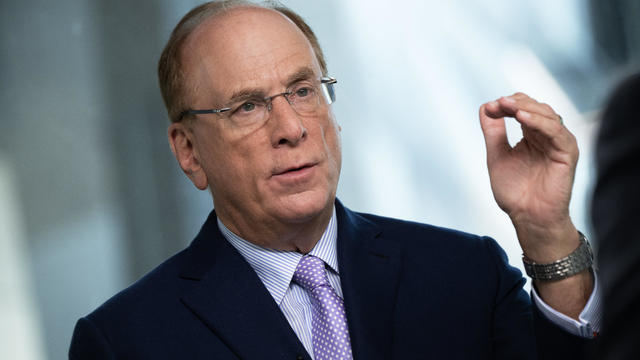

The U.S. is reaching "peak 65," marking the largest retirement wave in American history. But the financial outlook for many is grim.

Americans are underprepared for retirement, with the average account holding just $88,400 in savings.

BlackRock CEO Larry Fink said that longer life expectancies are "putting the U.S. retirement system under immense strain."

About 1 in 8 workers think they'll retire by age 61. But the reality of saving for decades of expenses is daunting.

Inflation-weary consumers have also been slammed by high borrowing costs. Here's what economists expect the Fed to announce.

Democratic state Sen. Timothy Kennedy won a special election for the New York congressional seat left vacant by Democrat Brian Higgins' departure from Congress.

Tuesday's storms came just two days after tornadoes tore through Oklahoma on Sunday, killing four people and injuring at least 100.

The FBI's searches, some of which were deemed to be improper in the past, were a flashpoint in a months-long fight in Congress over the reauthorization of Section 702 of FISA.

The woman was apparently trying to park her vehicle and stepped on the accelerator instead of the brakes, police said

Inflation-weary consumers have also been slammed by high borrowing costs. Here's what economists expect the Fed to announce.

Trump's ownership stake in Trump Media & Technology group now stands at $5.7 billion, buoyed by a rise in the stock's price.

Recall involves shelled walnuts distributed in 19 states and sold in bulk bins at natural food and co-op stores.

There's a new way to enroll in TSA PreCheck and skip long airport security lines. Here is where it's offered.

Friends will soon be able to bet against each other on who will win Skee-Ball.

Democratic state Sen. Timothy Kennedy won a special election for the New York congressional seat left vacant by Democrat Brian Higgins' departure from Congress.

The FBI's searches, some of which were deemed to be improper in the past, were a flashpoint in a months-long fight in Congress over the reauthorization of Section 702 of FISA.

The Biden administration is considering bringing certain Palestinians fleeing war-torn Gaza to the U.S. as refugees, according to internal federal government documents obtained by CBS News.

A motion in the Minnesota Senate to call for the resignation of bemired DFL Sen. Nicole Mitchell failed Tuesday. This came after a GOP-led effort to strip her of voting powers failed Monday.

The proposal would recognize the medical uses of cannabis and acknowledge it has less potential for abuse than some other drugs.

Recall involves shelled walnuts distributed in 19 states and sold in bulk bins at natural food and co-op stores.

Cat deaths and neurological disease are "widely reported" around farms where the H5N1 bird flu virus was detected, health officials say.

Methylene chloride, a toxic chemical, is linked to at least 88 deaths since 1980, federal regulators say.

In an abrupt switch, Walmart plans to shut 51 health clinics in six states and pull the plug on telemedicine services.

"It is against the basic civil and human rights that we have established are a key part of American identity," one advocate tells CBS News. "Community living should be the rule, rather than the exception."

"Life is so unfair to hit us where it hurts the most," former UFC champ Francis Ngannou said in a heartbreaking post.

The captain's behavior required an alternate crew be flown in from Japan, the airline said.

President William Ruto has promised help for Kenyans as unusually heavy monsoon rains burst a dam and unleash deadly floods and mudslides.

Britain's monarch, King Charles III, had put his official public duties on hold for weeks as he undergoes treatment for an unspecified cancer.

Social media video appeared to show the suspect trying to hide behind bushes while carrying a long bladed weapon.

See who's nominated for the 77th annual Tony Awards. The Tonys will air live on CBS and Paramount+ on Sunday, June 16.

Only on CBS Mornings, Tony Award-winning actors Jesse Tyler Ferguson and Renée Elise Goldsberry announced the nominations in six key categories for the 77th Annual Tony Awards.

Britain's monarch, King Charles III, had put his official public duties on hold for weeks as he undergoes treatment for an unspecified cancer.

Paramount said long-time CEO Bob Bakish will leave the company, which is in discussions to explore a sale or merger.

Justin Hartley stars as Colter Shaw, a rugged survivalist who traverses the country to locate missing people and collect rewards, in the new CBS show "Tracker."

Pollen counters are turning to artificial intelligence as seasonal allergies worsen due to climate change. CBS News national correspondent Dave Malkoff explains how technology is changing the long and tedious process of pollen counting.

Artificial intelligence assistants may soon be able to do much more than play your favorite music or call your mom, but some Google researchers warn about possible ethical dilemmas. CBS News reporter Erica Brown has more.

From labor shortages to environmental impacts, farmers are looking to AI to help revolutionize the agriculture industry. One California startup, Farm-ng, is tapping into the power of AI and robotics to perform a wide range of tasks, including seeding, weeding and harvesting.

A newly-filed lawsuit targets two of the biggest generative AI platforms in the world, Open AI, the creators of ChatGPT and Microsoft's Copilot AI program.

If you think allergies are worse this year, you aren't imagining it. CBS News correspondent Dave Malkoff shows us how a hyperlocal pollen count could help people manage symptoms better.

Pollen counters are turning to artificial intelligence as seasonal allergies worsen due to climate change. CBS News national correspondent Dave Malkoff explains how technology is changing the long and tedious process of pollen counting.

The bugs emit a loud, droning buzzing sound when they emerge – signaling they are ready to mate.

Officials from the National Weather Service and the CDC are already warning Americans about record-high temperatures in the coming months thanks to seasonal changes in the La Niña climate pattern. With these rising temperatures, there's also a higher risk of wildfires and droughts. Scott Dance, a climate reporter for The Washington Post, joined CBS News to discuss the forecast.

Bats have often been called scary and spooky but experts say they play an important role in our daily lives. CBS News' Danya Bacchus explains why the mammals are so vital to our ecosystem and the threats they're facing.

Pediatrician Dr. Mona Hanna-Attisha, whose work has spurred official action on the Flint water crisis, told CBS News that it's stunning that "we continue to use the bodies of our kids as detectors of environmental contamination." She discusses ways to support victims of the water crisis, the ongoing work of replacing the city's pipes and more in this extended interview.

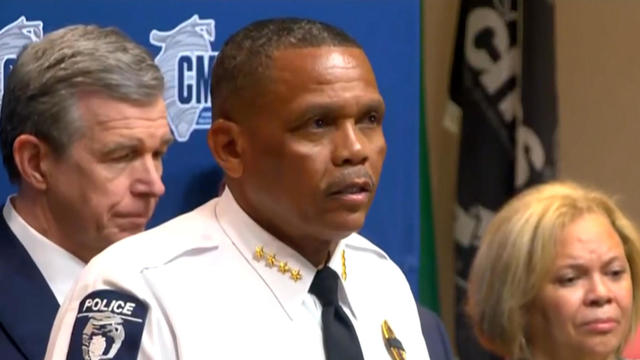

At least four law enforcement officers were killed during an operation in Charlotte, North Carolina, on Monday. Johnny Jennings, chief of the Charlotte-Mecklenburg Police Department, joins CBS News to discuss the case.

Four officers were killed Monday while trying to serve a warrant in Charlotte, North Carolina. The suspect, who was also killed, opened fire from the top floor of a house as the officers approached. Dave Malkoff has more on the slain officers.

Four law enforcement officers were killed and another four injured during a U.S. Marshals Service fugitive task force operation in Charlotte, North Carolina, Monday. A suspect was killed during the standoff, according to the Charlotte-Mecklenburg police chief. CBS News' Manuel Bojorquez has the latest confirmed information.

Authorities say they may have stopped a serial killer from striking again, after a man confessed to murdering two women.

Reports of elder fraud crimes increased by 14% in 2023, according to a new federal report.

The Horsehead Nebula, which NASA has called "one of the most distinctive objects in our skies," is located in the constellation Orion.

Astronauts Barry Wilmore and Sunita Williams say they have complete confidence in the Starliner despite questions about Boeing's safety culture.

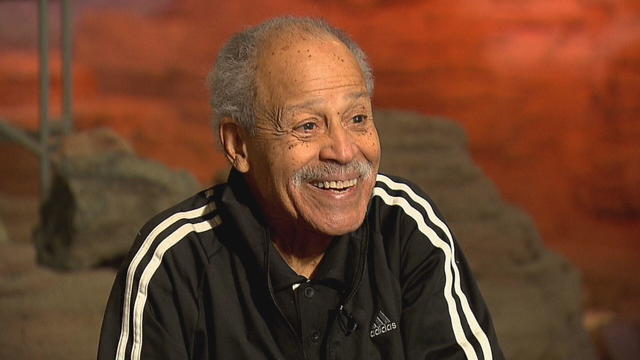

In 1961, Ed Dwight was selected by President John F. Kennedy to enter an Air Force training program known as the path to NASA's Astronaut Corps. But he ultimately never made it to space.

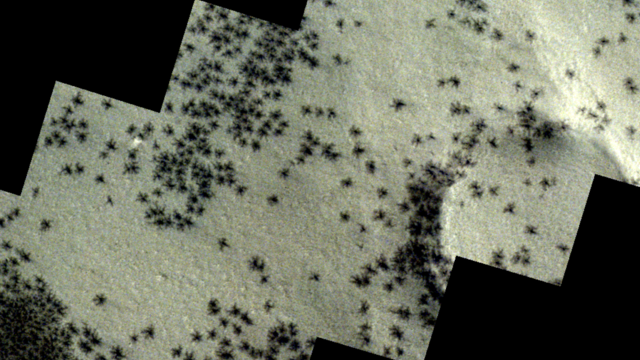

The creepy patterns were observed by the European Space Agency's ExoMars Trace Gas Orbiter.

The Shenzhou 18 crew will replace three taikonauts aboard the Chinese space station who are wrapping up a six-month stay.

A look back at the esteemed personalities who've left us this year, who'd touched us with their innovation, creativity and humanity.

The Francis Scott Key Bridge in Baltimore collapsed early Tuesday, March 26 after a column was struck by a container ship that reportedly lost power, sending vehicles and people into the Patapsco River.

When Tiffiney Crawford was found dead inside her van, authorities believed she might have taken her own life. But could she shoot herself twice in the head with her non-dominant hand?

We look back at the life and career of the longtime host of "Sunday Morning," and "one of the most enduring and most endearing" people in broadcasting.

Cayley Mandadi's mother and stepfather go to extreme lengths to prove her death was no accident.

Pollen counters are turning to artificial intelligence as seasonal allergies worsen due to climate change. CBS News national correspondent Dave Malkoff explains how technology is changing the long and tedious process of pollen counting.

Artificial intelligence assistants may soon be able to do much more than play your favorite music or call your mom, but some Google researchers warn about possible ethical dilemmas. CBS News reporter Erica Brown has more.

Israeli Prime Minister Benjamin Netanyahu says Israel will carry out an operation in the southern Gaza city of Rafah even if there is a cease-fire deal with Hamas. More than half of Gaza's population of 2.3 million people has been sheltering in Rafah from the war. Bob Kitchen, vice president of emergencies at the International Rescue Committee, joins CBS News to discuss the humanitarian crisis in the territory.

The White House is considering welcoming some Palestinians from Gaza into the U.S. as refugees. The Palestinians under consideration would include individuals with immediate family who are U.S. citizens or permanent residents.

Rep. Marjorie Taylor Greene is threatening to move ahead with a floor vote to remove Mike Johnson as House speaker. This comes after House Democrats announced Tuesday they would block the vote and save his job. CBS News congressional correspondent Nikole Killion has the details.