After Biden signs TikTok ban into law, ByteDance says it won't sell

The China-based owner of TikTok is facing a new law that will force it to either sell the wildly popular video platform, or face a U.S. ban.

Watch CBS News

The China-based owner of TikTok is facing a new law that will force it to either sell the wildly popular video platform, or face a U.S. ban.

Dutch medical device maker Philips says it's reached a $1.1 billion deal in the United States to settle lawsuits over faulty sleep machines in a case that's rocked the company.

Musk's surprise visit to the Beijing Auto Show this weekend was a "watershed moment" for Tesla, analysts said.

First known HIV cases from a nonsterile injection for cosmetic reasons highlights the risk of unlicensed providers.

With a relatively low average monthly cost of living and a low crime rate, this little-known town has a lot to offer retirees according to one report.

Intimacy coordination is a relatively new and growing field with movie and television productions required to make a good-faith effort to hire one if needed on set.

The Democratic Republic of Congo has given Apple weeks to answer questions about how it ensures key components in its tech are ethically and legally sourced.

Within three or four years, Aurora Innovation and its competitors expect to put thousands of self-driving trucks on America's public freeways. But the image of driverless semis on highways concerns many people, polls show.

Razer sold the Zephyr mask as protection against COVID during the pandemic, but products were not tested, feds say.

Long-term care insurance can be expensive if you're in your 70s. Here are ways to cut that cost.

There are a few compelling reasons that new investors, in particular, may want to buy gold bars now.

The window of opportunity to open a high-yield savings account has not closed yet. Here are three reasons why.

Tesla accounted for 80% of electric vehicle sales in the U.S. in 2020, but that figure fell to 55% last year.

The generative artificial intelligence boom has led to the emergence of romantic companion bots.

Apple said it will stop selling the devices later this month in order to comply with a U.S. import ban.

Alex Jones, the conspiracy theorist known for his fake news site InfoWars and his false denial of the Sandy Hook massacre, was permanently banned from Twitter in 2018.

More than 90 million consumers will scan a QR code this year. But the technology can also facilitate identity theft.

The billionaire owner of X took a defensive tone, saying that "the whole world will know that those advertisers killed the company."

OpenAI co-founder Sam Altman says he's looking forward to returning to the company, with the support of Microsoft's CEO, to build the 2 companies' "strong partnership."

Musk, who is under fire for supporting an antisemitic post, said the money will be donated to hospitals in Israel and to the Red Cross in Gaza.

Altman landed at Microsoft, the biggest investor in OpenAI, as former Twitch leader Emmett Shear was named OpenAI's new chief executive.

Ryan Watson is facing a potential sentence of 12 years behind bars in Turks and Caicos after four rounds of hunting ammunition were found in his luggage.

The Charlotte-Mecklenburg Police Department said on social media the officers were taken to a hospital.

Columbia University told students protesting they must clear the encampment by 2 p.m. Monday or they will face suspension.

The Democratic Republic of Congo has given Apple weeks to answer questions about how it ensures key components in its tech are ethically and legally sourced.

The Supreme Court on Monday declined former White House trade adviser Peter Navarro's request to halt his prison sentence while he appeals a conviction for contempt of Congress.

Delta Air Lines appears to have recovered the emergency slide that fell from a plane minutes after takeoff at JFK in the Rockaways.

Cartier ultimately agreed to let the buyer keep the earrings he had purchased at an inadvertent discount. Not everyone supports the outcome.

Indian parliamentarian Prajwal Revanna, whose party is allied with the prime minister, is accused of recording thousands of videos of sexual assault.

Fine dining at Disney? Theme park is now home to one of 26 Florida restaurants awarded a coveted star from the Michelin Guide.

With a relatively low average monthly cost of living and a low crime rate, this little-known town has a lot to offer retirees according to one report.

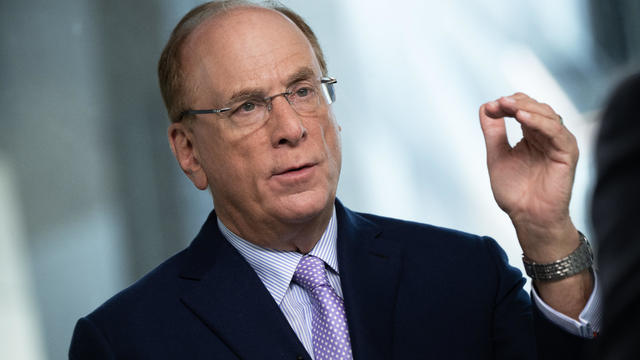

The U.S. is reaching "peak 65," marking the largest retirement wave in American history. But the financial outlook for many is grim.

Americans are underprepared for retirement, with the average account holding just $88,400 in savings.

BlackRock CEO Larry Fink said that longer life expectancies are "putting the U.S. retirement system under immense strain."

About 1 in 8 workers think they'll retire by age 61. But the reality of saving for decades of expenses is daunting.

Razer sold the Zephyr mask as protection against COVID during the pandemic, but products were not tested, feds say.

The Charlotte-Mecklenburg Police Department said on social media the officers were taken to a hospital.

Ryan Watson is facing a potential sentence of 12 years behind bars in Turks and Caicos after four rounds of hunting ammunition were found in his luggage.

Cartier ultimately agreed to let the buyer keep the earrings he had purchased at an inadvertent discount. Not everyone supports the outcome.

The pistol that notorious Chicago gangster Al Capone supposedly called his "favorite" gun is up for auction in South Carolina next month.

Razer sold the Zephyr mask as protection against COVID during the pandemic, but products were not tested, feds say.

Cartier ultimately agreed to let the buyer keep the earrings he had purchased at an inadvertent discount. Not everyone supports the outcome.

Musk's surprise visit to the Beijing Auto Show this weekend was a "watershed moment" for Tesla, analysts said.

The Democratic Republic of Congo has given Apple weeks to answer questions about how it ensures key components in its tech are ethically and legally sourced.

The pistol that notorious Chicago gangster Al Capone supposedly called his "favorite" gun is up for auction in South Carolina next month.

The Supreme Court on Monday declined former White House trade adviser Peter Navarro's request to halt his prison sentence while he appeals a conviction for contempt of Congress.

Columbia University told students protesting they must clear the encampment by 2 p.m. Monday or they will face suspension.

It's the first meeting between the two men since Florida Governor Ron DeSantis ended his 2024 presidential challenge against former President Trump.

South Dakota Gov. Kristi Noem addressed on social media the backlash she received after details of her soon-to-be-released book were revealed.

Campus protesters are "looking for some sort of acknowledgement from our leadership," Democratic Rep. Summer Lee of Pennsylvania said.

Razer sold the Zephyr mask as protection against COVID during the pandemic, but products were not tested, feds say.

Dutch medical device maker Philips says it's reached a $1.1 billion deal in the United States to settle lawsuits over faulty sleep machines in a case that's rocked the company.

Oregon is helping Medicaid patients cope with soaring heat, smoky skies and other effects of climate change.

Around 1 in 5 retail milk samples had tested positive for the bird flu virus, but further tests show it was not infectious.

The White House had been due to decide on the menthol cigarette rule in March.

It's invasive, harmful and can regenerate from a tiny piece of its body — it's the hammerhead land planarian, and its been increasingly sighted in Ontario.

Ryan Watson is facing a potential sentence of 12 years behind bars in Turks and Caicos after four rounds of hunting ammunition were found in his luggage.

Musk's surprise visit to the Beijing Auto Show this weekend was a "watershed moment" for Tesla, analysts said.

The Democratic Republic of Congo has given Apple weeks to answer questions about how it ensures key components in its tech are ethically and legally sourced.

Indian parliamentarian Prajwal Revanna, whose party is allied with the prime minister, is accused of recording thousands of videos of sexual assault.

Justin Hartley stars as Colter Shaw, a rugged survivalist who traverses the country to locate missing people and collect rewards, in the new CBS show "Tracker."

Justin Hartley returns to television as both star and executive producer of "Tracker," an action-packed drama where he plays Colter Shaw, a survivalist hunting for missing persons across the country.

Known as "The Man of Many Voices," 25-year-old comedian Matt Friend delivered a standout performance at the White House Correspondents' Dinner, showcasing his talent with 250 impressions of famous figures.

French screen actor Gerard Depardieu has reportedly been detained for questioning after two women accused him of sexual assault.

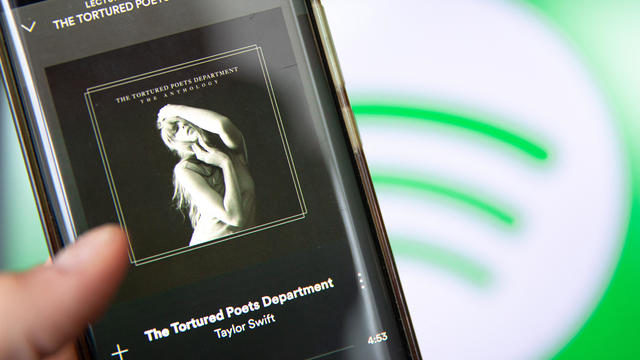

The vinyl sales alone were monumental, Billboard said, with "the largest sales week for an album on vinyl in the modern era."

After delving into the world of romance scams, CBS News followed up with several victims whose ordeals were highlighted. Jim Axelrod shares their stories.

NYU Langone Health and Meta have developed a new type of MRI that dramatically reduces the time needed to complete scans through artificial intelligence. CBS News correspondent Anne-Marie Green reports.

From labor shortages to environmental impacts, farmers are looking to AI to help revolutionize the agriculture industry. One California startup, Farm-ng, is tapping into the power of AI and robotics to perform a wide range of tasks, including seeding, weeding and harvesting.

The Federal Communications Commission voted to adopt net neutrality regulations, a reversal from the policy adopted during former President Donald Trump's administration. Christopher Sprigman, a professor at the New York University School of Law, joins CBS News with more on the vote.

Are you using your smartwatch to the fullest? Here are 4 metrics doctors say can be useful to track beyond your daily step count.

Officials from the National Weather Service and the CDC are already warning Americans about record-high temperatures in the coming months thanks to seasonal changes in the La Niña climate pattern. With these rising temperatures, there's also a higher risk of wildfires and droughts. Scott Dance, a climate reporter for The Washington Post, joined CBS News to discuss the forecast.

Bats have often been called scary and spooky but experts say they play an important role in our daily lives. CBS News' Danya Bacchus explains why the mammals are so vital to our ecosystem and the threats they're facing.

Pediatrician Dr. Mona Hanna-Attisha, whose work has spurred official action on the Flint water crisis, told CBS News that it's stunning that "we continue to use the bodies of our kids as detectors of environmental contamination." She discusses ways to support victims of the water crisis, the ongoing work of replacing the city's pipes and more in this extended interview.

Ten years ago, a water crisis began when Flint, Michigan, switched to the Flint River for its municipal water supply. The more corrosive water was not treated properly, allowing lead from pipes to leach into many homes. CBS News correspondent Ash-har Quraishi spoke with residents about what the past decade has been like.

According to the University of California, Davis, residential energy use is responsible for 20% of total greenhouse gas emissions in the U.S. However, one company is helping residential buildings reduce their impact and putting carbon to use. CBS News' Bradley Blackburn shows how the process works.

The Charlotte-Mecklenburg Police Department said on social media the officers were taken to a hospital.

Indian parliamentarian Prajwal Revanna, whose party is allied with the prime minister, is accused of recording thousands of videos of sexual assault.

Opening statements are set to begin this morning in the murder trial for Karen Read, the Massachusetts woman accused of killing her police officer boyfriend in 2022. Read's lawyers claim that she is being framed as part of a cover-up and she has pleaded not guilty to all charges. CBS News Boston reporter Penny Kmitt has more.

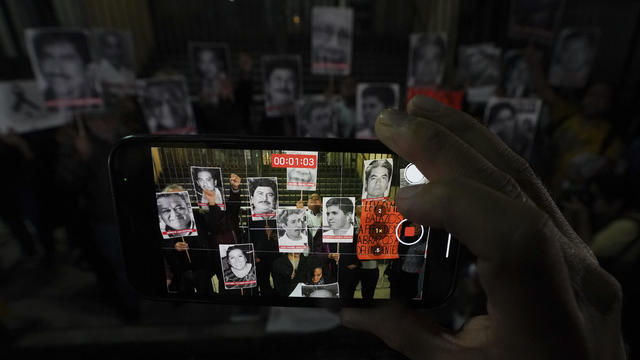

Media workers are regularly targeted in Mexico, often in direct reprisal for their work covering corruption and drug traffickers.

After delving into the world of romance scams, CBS News followed up with several victims whose ordeals were highlighted. Jim Axelrod shares their stories.

Astronauts Barry Wilmore and Sunita Williams say they have complete confidence in the Starliner despite questions about Boeing's safety culture.

In 1961, Ed Dwight was selected by President John F. Kennedy to enter an Air Force training program known as the path to NASA's Astronaut Corps. But he ultimately never made it to space.

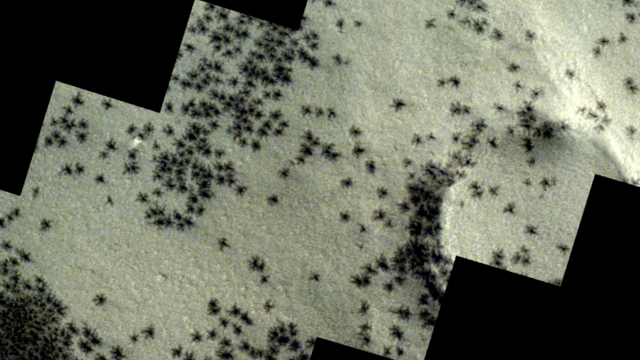

The creepy patterns were observed by the European Space Agency's ExoMars Trace Gas Orbiter.

The Shenzhou 18 crew will replace three taikonauts aboard the Chinese space station who are wrapping up a six-month stay.

In November 2023, NASA's Voyager 1 spacecraft stopped sending "readable science and engineering data."

A look back at the esteemed personalities who've left us this year, who'd touched us with their innovation, creativity and humanity.

The Francis Scott Key Bridge in Baltimore collapsed early Tuesday, March 26 after a column was struck by a container ship that reportedly lost power, sending vehicles and people into the Patapsco River.

When Tiffiney Crawford was found dead inside her van, authorities believed she might have taken her own life. But could she shoot herself twice in the head with her non-dominant hand?

We look back at the life and career of the longtime host of "Sunday Morning," and "one of the most enduring and most endearing" people in broadcasting.

Cayley Mandadi's mother and stepfather go to extreme lengths to prove her death was no accident.

Multiple law enforcement officers were shot in Charlotte, North Carolina, Monday during an investigation, police said. CBS affiliate WBTV is following the latest.

Ryan Watson, an American tourist detained in Turks and Caicos after officials there discovered ammo in his luggage, is speaking out. Watson, who is out on bail after being arrested, tells CBS News he was not aware of the ammo in his possessions.

At least four people were killed and more than a hundred injured when a string of tornadoes tore through Oklahoma, ripping homes apart and battering entire communities. CBS News correspondent Omar Villafranca reports from Sulphur.

Susie Wolff, a pioneering figure in motorsports, made history as the first woman in more than 20 years to participate in a Formula One race weekend. She joins "CBS Mornings" to discuss her career and current role as the managing director of the all-female F1 Academy.

Columbia University set a new deadline for pro-Palestinian protesters to clear out the encampment on the campus Monday after announcing the institution will not divest from Israel. CBS News' Tom Hanson is following the latest.