Walmart is launching an upscale store brand. Here what it's selling.

Walmart said its new store brand Bettergoods is "chef-inspired," and offers dozens of upscale products like plant-based milks.

Watch CBS News

Walmart said its new store brand Bettergoods is "chef-inspired," and offers dozens of upscale products like plant-based milks.

Voters rank the economy ahead of other hot button topics as one of the most important issues ahead of the 2024 presidential election.

USDA says the U.S. meat supply is safe, and reiterates that people should cook beef to kill bacteria and viruses.

Paramount said its long-time CEO, Bob Bakish, will leave the company, which is in discussions to explore a sale or merger.

Cartier ultimately agreed to let the buyer keep the earrings he had purchased at an inadvertent discount. Not everyone supports the outcome.

Fine dining at Disney? Theme park is now home to one of 26 Florida restaurants awarded a coveted star from the Michelin Guide.

The China-based owner of TikTok is facing a new law that will force it to either sell the wildly popular video platform, or face a U.S. ban.

Razer sold the Zephyr mask as protection against COVID during the pandemic, but products were not tested, feds say.

Reports of elder fraud crimes increased by 14% in 2023, according to a new federal report.

There are many gold asset options to invest in, but 1-ounce gold bars could make sense for seniors right now.

Debt consolidation loans and debt consolidation programs can help you get out of debt. But which is better?

Here's what could happen to home equity loan rates after this week's Federal Reserve meeting.

Tesla accounted for 80% of electric vehicle sales in the U.S. in 2020, but that figure fell to 55% last year.

The generative artificial intelligence boom has led to the emergence of romantic companion bots.

Apple said it will stop selling the devices later this month in order to comply with a U.S. import ban.

Alex Jones, the conspiracy theorist known for his fake news site InfoWars and his false denial of the Sandy Hook massacre, was permanently banned from Twitter in 2018.

More than 90 million consumers will scan a QR code this year. But the technology can also facilitate identity theft.

The billionaire owner of X took a defensive tone, saying that "the whole world will know that those advertisers killed the company."

OpenAI co-founder Sam Altman says he's looking forward to returning to the company, with the support of Microsoft's CEO, to build the 2 companies' "strong partnership."

Musk, who is under fire for supporting an antisemitic post, said the money will be donated to hospitals in Israel and to the Red Cross in Gaza.

Altman landed at Microsoft, the biggest investor in OpenAI, as former Twitch leader Emmett Shear was named OpenAI's new chief executive.

The third week of former President Donald Trump's New York criminal trial kicked off Tuesday with rulings from the judge and continued testimony.

Dozens of protesters took over a building at Columbia University in New York in the latest escalation of demonstrations against the Israel-Hamas war that have spread to college campuses nationwide.

Judge Juan Merchan said Trump violated the order nine times in recent weeks and fined him $1,000 for each violation.

See who's nominated for the 77th annual Tony Awards. The Tonys will air live on CBS and Paramount+ on Sunday, June 16.

A U.S. Marshals Service fugitive task force was attempting to serve a warrant in Charlotte when the shooting started, the police said.

The captain's behavior required an alternate crew be flown in from Japan, the airline said.

Last summer, hundreds of millions of people were faced with triple-digit temperatures across the U.S. This year, it could happen again.

If Rep. Majorie Tayler Greene invokes the motion the vacate, "it will not succeed," House Democrats said in a statement Tuesday.

A toddler suffered serious injuries while playing in a bounce house that was lifted off the ground by wind gusts near Phoenix. He later died.

With a relatively low average monthly cost of living and a low crime rate, this little-known town has a lot to offer retirees according to one report.

The U.S. is reaching "peak 65," marking the largest retirement wave in American history. But the financial outlook for many is grim.

Americans are underprepared for retirement, with the average account holding just $88,400 in savings.

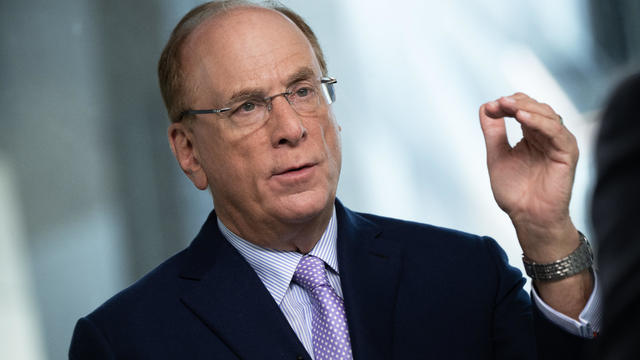

BlackRock CEO Larry Fink said that longer life expectancies are "putting the U.S. retirement system under immense strain."

About 1 in 8 workers think they'll retire by age 61. But the reality of saving for decades of expenses is daunting.

Last summer, hundreds of millions of people were faced with triple-digit temperatures across the U.S. This year, it could happen again.

Alexa Curtis' accomplishment was not met with many congratulations – because she also admitted she didn't register for the race, a practice called "banditing."

The captain's behavior required an alternate crew be flown in from Japan, the airline said.

Some of the names coming up most consistently have been on Trump's list for months, while other candidates seem to be sliding out of favor.

"They looked me in the eye and told me… 'We would never poison our own people,'" one former water resource management commissioner said. "And they lied. They lied about all of it."

Reports of elder fraud crimes increased by 14% in 2023, according to a new federal report.

Walmart said its new store brand Bettergoods is "chef-inspired," and offers dozens of upscale products like plant-based milks.

Voters rank the economy ahead of other hot button topics as one of the most important issues ahead of the 2024 presidential election.

USDA says the U.S. meat supply is safe, and reiterates that people should cook beef to kill bacteria and viruses.

Paramount said long-time CEO Bob Bakish will leave the company, which is in discussions to explore a sale or merger.

With economic development at the forefront, the Biden campaign is tapping Vice President Kamala Harris to win over Black voters.

Some of the names coming up most consistently have been on Trump's list for months, while other candidates seem to be sliding out of favor.

If Rep. Majorie Tayler Greene invokes the motion the vacate, "it will not succeed," House Democrats said in a statement Tuesday.

Reports of elder fraud crimes increased by 14% in 2023, according to a new federal report.

Judge Juan Merchan said Trump violated the order nine times in recent weeks and fined him $1,000 for each violation.

"It is against the basic civil and human rights that we have established are a key part of American identity," one advocate tells CBS News. "Community living should be the rule, rather than the exception."

Unlike pasteurized milk, which undergoes a process that kills harmful bacteria, experts say raw milk can carry pathogens that make you sick.

USDA says the U.S. meat supply is safe, and reiterates that people should cook beef to kill bacteria and viruses.

Razer sold the Zephyr mask as protection against COVID during the pandemic, but products were not tested, feds say.

Dutch medical device maker Philips says it's reached a $1.1 billion deal in the United States to settle lawsuits over faulty sleep machines in a case that's rocked the company.

The captain's behavior required an alternate crew be flown in from Japan, the airline said.

President William Ruto has promised help for Kenyans as unusually heavy monsoon rains burst a dam and unleash deadly floods and mudslides.

Britain's monarch, King Charles III, had put his official public duties on hold for weeks as he undergoes treatment for an unspecified cancer.

Social media video appeared to show the suspect trying to hide behind bushes while carrying a long bladed weapon.

Columbia University protesters have set up a new demonstration at Hamilton Hall, a building demonstrators occupied during 1968 anti-Vietnam war protests.

See who's nominated for the 77th annual Tony Awards. The Tonys will air live on CBS and Paramount+ on Sunday, June 16.

Only on CBS Mornings, Tony Award-winning actors Jesse Tyler Ferguson and Renée Elise Goldsberry announced the nominations in six key categories for the 77th Annual Tony Awards.

Britain's monarch, King Charles III, had put his official public duties on hold for weeks as he undergoes treatment for an unspecified cancer.

Paramount said long-time CEO Bob Bakish will leave the company, which is in discussions to explore a sale or merger.

Justin Hartley stars as Colter Shaw, a rugged survivalist who traverses the country to locate missing people and collect rewards, in the new CBS show "Tracker."

The U.S. is ramping up its chip production while trying to block China from dominating the market.

After delving into the world of romance scams, CBS News followed up with several victims whose ordeals were highlighted. Jim Axelrod shares their stories.

From labor shortages to environmental impacts, farmers are looking to AI to help revolutionize the agriculture industry. One California startup, Farm-ng, is tapping into the power of AI and robotics to perform a wide range of tasks, including seeding, weeding and harvesting.

NYU Langone Health and Meta have developed a new type of MRI that dramatically reduces the time needed to complete scans through artificial intelligence. CBS News correspondent Anne-Marie Green reports.

The Federal Communications Commission voted to adopt net neutrality regulations, a reversal from the policy adopted during former President Donald Trump's administration. Christopher Sprigman, a professor at the New York University School of Law, joins CBS News with more on the vote.

The bugs emit a loud, droning buzzing sound when they emerge – signaling they are ready to mate.

Officials from the National Weather Service and the CDC are already warning Americans about record-high temperatures in the coming months thanks to seasonal changes in the La Niña climate pattern. With these rising temperatures, there's also a higher risk of wildfires and droughts. Scott Dance, a climate reporter for The Washington Post, joined CBS News to discuss the forecast.

Bats have often been called scary and spooky but experts say they play an important role in our daily lives. CBS News' Danya Bacchus explains why the mammals are so vital to our ecosystem and the threats they're facing.

Pediatrician Dr. Mona Hanna-Attisha, whose work has spurred official action on the Flint water crisis, told CBS News that it's stunning that "we continue to use the bodies of our kids as detectors of environmental contamination." She discusses ways to support victims of the water crisis, the ongoing work of replacing the city's pipes and more in this extended interview.

Ten years ago, a water crisis began when Flint, Michigan, switched to the Flint River for its municipal water supply. The more corrosive water was not treated properly, allowing lead from pipes to leach into many homes. CBS News correspondent Ash-har Quraishi spoke with residents about what the past decade has been like.

Reports of elder fraud crimes increased by 14% in 2023, according to a new federal report.

Witness testimony continues Tuesday in the murder trial of Karen Read, a woman accused in the death of her Boston police officer boyfriend. Read's defense team argues she is the victim of an elaborate cover-up and is being framed by a group of people that includes law enforcement while prosecutors claim she hit officer John O'Keefe with her vehicle during a snowstorm in 2022.

The death of 49-year-old Suzanne Morphew, a Colorado mother who went missing over three years ago, has been officially declared a homicide, according to a newly released autopsy report. This revelation comes two years after prosecutors dropped murder charges against her husband just as he was about to stand trial.

On Monday, the court heard opening statements in the trial of Karen Read, who has pleaded not guilty to second degree murder for the 2022 death of her police officer boyfriend in Massachusetts. On Tuesday, the defense will cross-examine the first officer who was on scene. Dozens of witnesses are expected to testify.

Social media video appeared to show the suspect trying to hide behind bushes while carrying a long bladed weapon.

The Horsehead Nebula, which NASA has called "one of the most distinctive objects in our skies," is located in the constellation Orion.

Astronauts Barry Wilmore and Sunita Williams say they have complete confidence in the Starliner despite questions about Boeing's safety culture.

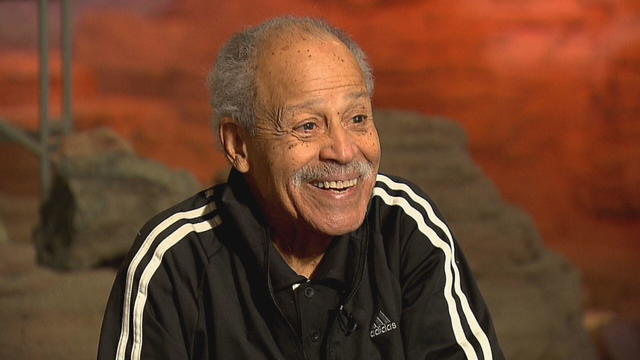

In 1961, Ed Dwight was selected by President John F. Kennedy to enter an Air Force training program known as the path to NASA's Astronaut Corps. But he ultimately never made it to space.

The creepy patterns were observed by the European Space Agency's ExoMars Trace Gas Orbiter.

The Shenzhou 18 crew will replace three taikonauts aboard the Chinese space station who are wrapping up a six-month stay.

A look back at the esteemed personalities who've left us this year, who'd touched us with their innovation, creativity and humanity.

The Francis Scott Key Bridge in Baltimore collapsed early Tuesday, March 26 after a column was struck by a container ship that reportedly lost power, sending vehicles and people into the Patapsco River.

When Tiffiney Crawford was found dead inside her van, authorities believed she might have taken her own life. But could she shoot herself twice in the head with her non-dominant hand?

We look back at the life and career of the longtime host of "Sunday Morning," and "one of the most enduring and most endearing" people in broadcasting.

Cayley Mandadi's mother and stepfather go to extreme lengths to prove her death was no accident.

If you think allergies are worse this year, you aren't imagining it. CBS News correspondent Dave Malkoff shows us how a hyperlocal pollen count could help people manage symptoms better.

The House Rules Committee has advanced a bipartisan bill that aims to define antisemitism. The House is expected to vote on the legislation this week. CBS News congressional correspondent Nikole Killion has the latest.

CBS News polling shows support for the Biden administration has dipped among Black Americans since 2020. The Biden reelection campaign has been trying to work on that with Vice President Kamala Harris meeting with Black business owners in Atlanta on Monday. Congressman Steven Horsford, the chair of the Congressional Black Caucus who was in Atlanta with Harris, joined CBS News to discuss the 2024 election.

Israel has offered Hamas what it described as a generous deal for a cease-fire and the release of hostages in Gaza, but snags remain and officials involved with the talks are wary of optimism. CBS News intelligence and national security reporter Olivia Gazis has more.

Officials in North Carolina provided an update Tuesday on the four officers who were shot and killed Monday while serving a warrant. CBS News national correspondent Manuel Bojorquez gave an update on the situation following the press conference.