Here's how to get a tax extension from the IRS in 2024

If you're one of the millions of taxpayers who delay their taxes, it's easy to get an extension to October 15.

Watch CBS News

If you're one of the millions of taxpayers who delay their taxes, it's easy to get an extension to October 15.

The former president's media company has had a rough welcome on Wall Street, shedding two-thirds of its value since its peak.

The tax-prep software giant says it has resolved an issue that blocked some customers from e-filing on Sunday and much of Monday.

"It must be done," Tesla CEO Elon Musk said in a memo about the layoffs sent to employees on Sunday.

The housing market continues to be challenging for both buyers and sellers this year, as mortgage rates and asking prices continue to climb

After passing easily in the House, a bill that would have expanded the CTC is stalled in the Senate. Here's what to know.

Dream condiment now a reality: Heinz Classic Barbiecue Sauce available in the U.K. and Spain. Will "Kenchup" be next?

Nike's unitard for female track and field athletes representing the U.S. at the 2024 Paris Olympics is too revealing, critics say.

As Americans race to file their returns on Tax DAy, restaurant chains and other businesses are offering a range of deals.

Gold bars and coins could be worth pursuing now that inflation is on the rise again.

There are options for tapping into your home's equity even if your mortgage loan is paid off. Here's what to know.

With inflation rising again, it makes sense to take advantage of what a high-rate CD can offer now.

Tesla accounted for 80% of electric vehicle sales in the U.S. in 2020, but that figure fell to 55% last year.

The generative artificial intelligence boom has led to the emergence of romantic companion bots.

Apple said it will stop selling the devices later this month in order to comply with a U.S. import ban.

Alex Jones, the conspiracy theorist known for his fake news site InfoWars and his false denial of the Sandy Hook massacre, was permanently banned from Twitter in 2018.

More than 90 million consumers will scan a QR code this year. But the technology can also facilitate identity theft.

The billionaire owner of X took a defensive tone, saying that "the whole world will know that those advertisers killed the company."

OpenAI co-founder Sam Altman says he's looking forward to returning to the company, with the support of Microsoft's CEO, to build the 2 companies' "strong partnership."

Musk, who is under fire for supporting an antisemitic post, said the money will be donated to hospitals in Israel and to the Red Cross in Gaza.

Altman landed at Microsoft, the biggest investor in OpenAI, as former Twitch leader Emmett Shear was named OpenAI's new chief executive.

A fourth body was recovered Sunday at the site of the Key Bridge collapse, according to the Unified Command.

The first criminal trial of a former president in U.S. history officially got underway in a crowded Manhattan courtroom, where jury selection has begun.

"I dreamed of this moment since I was in second grade," Clark said.

The fallout from the Jan. 6, 2021, attack will land before the Supreme Court on Tuesday when the justices consider the scope of a federal obstruction statute.

The House speaker says he wants to put up separate individual bills on aid for Ukraine, Israel, and Taiwan.

Idaho Gov. Brad Little, a Republican, signed a bill into law last year that prohibits gender-affirming medical treatments for transgender minors.

Hannah Gutierrez-Reed, the armorer on Alec Baldwin's film "Rust," was given the maximum sentence of 18 months in prison for involuntary manslaughter.

Amid complaints about alleged antisemitic views posted online, USC's valedictorian will not be permitted to deliver a speech at the university's commencement ceremony due to concerns about security, the school's provost announced today.

Details emerge of Iran's unprecedented direct attack on Israel, and how it was largely thwarted by the U.S. ally's defenses.

Former "Monty Python" star Eric Idle said people "always assume we're loaded." He added, "I have to work for my living."

Only about 1 in 10 Americans understands the basics of longevity, or how long they'll live in retirement. Can you pass the test?

Over the next few years, the U.S. could see a surge in seniors living in poverty, one retirement expert predicts.

The gap between what people think they'll need for old age and their actual savings is massive, even for those nearing retirement.

Seniors and other recipients of the Social Security program may get a cost-of-living adjustment of 3.1% next year, one forecast says.

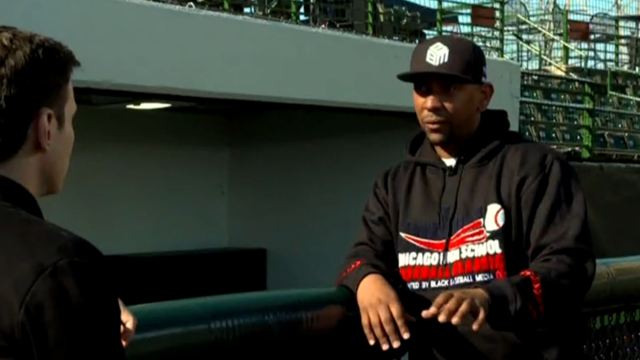

Earnest Horton founded Black Baseball Media, which gives players from predominantly underserved communities access to top-notch facilities and exposure to college scouts.

Caitlin Clark has been selected with the No. 1 pick in the WNBA draft by the Indiana Fever.

The housing market continues to be challenging for both buyers and sellers this year, as mortgage rates and asking prices continue to climb

The tax-prep software giant says it has resolved an issue that blocked some customers from e-filing on Sunday and much of Monday.

Idaho Gov. Brad Little, a Republican, signed a bill into law last year that prohibits gender-affirming medical treatments for transgender minors.

The housing market continues to be challenging for both buyers and sellers this year, as mortgage rates and asking prices continue to climb

The tax-prep software giant says it has resolved an issue that blocked some customers from e-filing on Sunday and much of Monday.

Nike's unitard for female track and field athletes representing the U.S. at the 2024 Paris Olympics is too revealing, critics say.

The former president's media company has had a rough start on Wall Street, shedding two-thirds of its value since its peak.

Dream condiment now a reality: Heinz Classic Barbiecue Sauce available in the U.K. and Spain. Will "Kenchup" be next?

The House speaker says he wants to put up separate individual bills on aid for Ukraine, Israel, and Taiwan.

Idaho Gov. Brad Little, a Republican, signed a bill into law last year that prohibits gender-affirming medical treatments for transgender minors.

Iran's attack on Israel has renewed urgency in getting a Senate-passed bill through the House. But the bill also threatens Johnson's speakership.

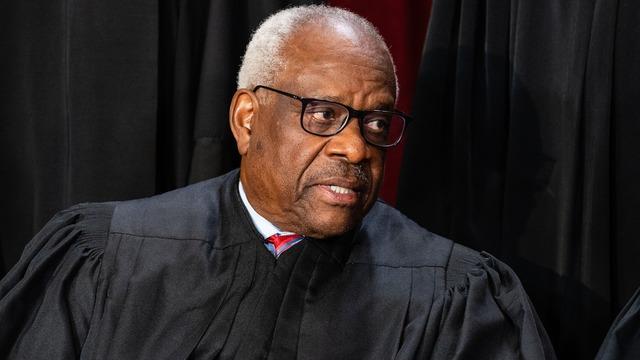

Justice Clarence Thomas did not attend oral arguments at the Supreme Court on Monday.

The fallout from the Jan. 6, 2021, attack will land before the Supreme Court on Tuesday when the justices consider the scope of a federal obstruction statute.

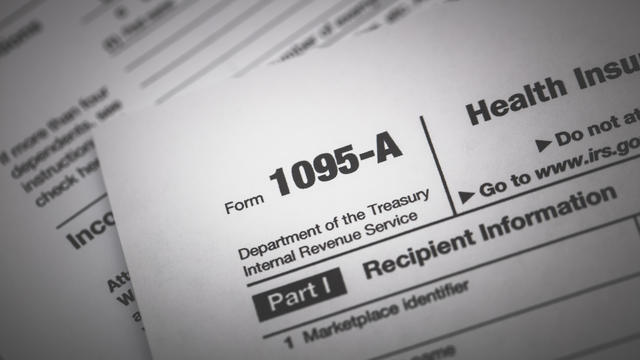

Consumer complaints have risen in recent months of unauthorized enrollment in Affordable Care Act coverage.

Social services, such as parenting classes and economic development programs, can help, some health experts say. But insurers don't always cover these services.

George Schappell and sister Lori, of Reading, Pa., were the world's oldest conjoined twins, according to the Guinness Book of World Records.

Vice President Kamala Harris campaigned in Arizona Friday, where she blamed former President Donald Trump for the Arizona Supreme Court ruling earlier this week which could pave the way to revive a near-total abortion ban. Janet Shamlian has more.

Federal authorities are warning that unregulated Botox products are linked to an outbreak of botulism-like illnesses.

The House speaker says he wants to put up separate individual bills on aid for Ukraine, Israel, and Taiwan.

Iran's attack on Israel has renewed urgency in getting a Senate-passed bill through the House. But the bill also threatens Johnson's speakership.

American carpenter Hank Silver on why he couldn't turn down an opportunity to help resurrect Paris' Notre Dame cathedral from a devastating fire.

A now-viral video shows three other runners in a pack with Chinese runner Jie He, and one appears to wave him over just before the finish line.

Details emerge of Iran's unprecedented direct attack on Israel, and how it was largely thwarted by the U.S. ally's defenses.

A Billy Joel special on CBS and Paramount+ will air again after it was cut off in the middle of the singer's performance of "Piano Man."

This week on CBS’s hit comedy "Ghosts," Rebecca Wisocky returns as the Gilded Age socialite Hetty, revealing surprising details about her character's past.

The comedian has stepped into his director's shoes for his new film, the not-quite-true story of the creation of the Kellogg's Pop-Tart.

Comedian Jerry Seinfeld has stepped into the director's shoes for his new Netflix film "Unfrosted," the not-quite-true story of the creation of the Kellogg's Pop-Tart. Correspondent Mo Rocca talks with Seinfeld about working behind the camera for the first time, and calling on a bunch of his comedian friends (including "Sunday Morning" contributor Jim Gaffigan) to act in his origin tale of a breakfast staple.

At the age of 28, Tyler Henry has become one of the best-known psychics anywhere, with a TV show, a road show and, he says, a 600,000-plus waiting list of people who want him to help them connect with their departed loved ones. Correspondent Tracy Smith sits down with Henry to discuss how he first recognized his ability at the age of 10; why he welcomes skepticism; and how he believes his talent helps people deal with grief.

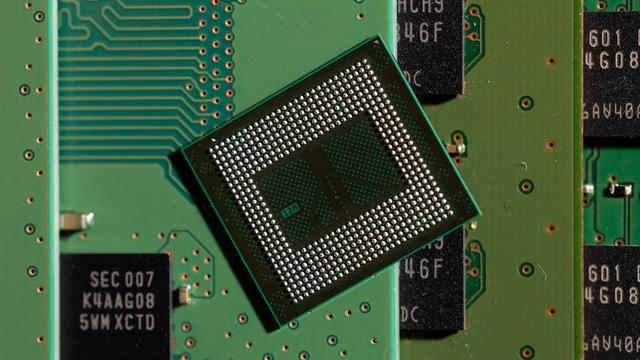

The Biden administration is awarding Samsung $6.4 billion to expand American chipmaking. The company will spread the money across at least five facilities in Texas. Sujai Shivakumar, senior fellow at the Center for Strategic and International Studies, joins CBS News to assess the economic and technological impacts.

Roku said Friday a second security breach impacted more than 576,000 accounts after announcing in March that 15,000 accounts had been exposed by a hack. Emma Roth, a writer for The Verge, joins CBS News with more details.

From labor shortages to environmental impacts, farmers are looking to AI to help revolutionize the agriculture industry. One California startup, Farm-ng, is tapping into the power of AI and robotics to perform a wide range of tasks, including seeding, weeding and harvesting.

The bill reforms and extends a portion of the Foreign Intelligence Surveillance Act known as Section 702 for a shortened period of two years.

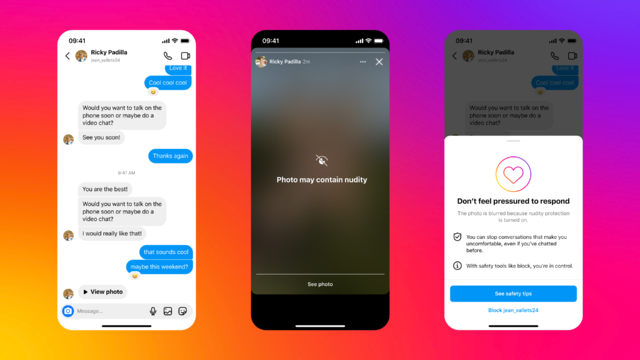

The feature will be turned on by default globally for teens under 18. Adult users will get a notification encouraging them to activate it, Meta said.

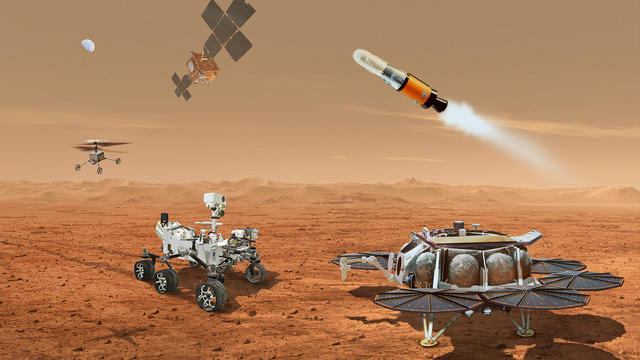

NASA said it agrees with an independent review board that concluded the project could cost up to $11 billion without major changes.

Only 5 to 6% of plastic waste produced in the U.S. is actually recycled. A new report accuses the plastics industry of a decades-long campaign to "mislead" the public about the viability of recycling.

Mexico City, one of the world's most populated cities with nearly 22 million people, could run out of water in months. Florencia Gonzalez Guerra, an investigative video journalist, joins CBS News to examine the causes behind the crisis.

Greenhouse gas emissions continued increasing in 2023, according to new data from the National Oceanic and Atmospheric Administration. CBS News' Elaine Quijano breaks down the numbers and what they mean for the climate.

The Biden administration awarded $830 million Thursday to fund projects that will address the impact of climate change on America's aging infrastructure. Ali Zaidi, an assistant to the president and national climate adviser, joins CBS News with more on the funding.

Hannah Gutierrez-Reed, the "Rust" Western film armorer who last month was found guilty of involuntary manslaughter in the deadly shooting of the film's cinematographer Halyna Hutchins, was sentenced to 18 months in prison for her part in the 2021 incident. CBS News legal contributor Jessica Levinson breaks down the sentencing.

Hannah Gutierrez-Reed, the armorer on Alec Baldwin's film "Rust," was given the maximum sentence of 18 months in prison for involuntary manslaughter.

A teenager has been arrested after a stabbing attack in a church in a Sydney suburb that officials Monday called "a terrorist incident."

Federal authorities are asking for the public's help in tracking down two men seen damaging popular rock formations at the Lake Mead National Recreation Area in Nevada.

The first criminal trial of a former president in U.S. history officially got underway in a crowded Manhattan courtroom, where jury selection has begun.

NASA said it agrees with an independent review board that concluded the project could cost up to $11 billion without major changes.

It was a "bittersweet moment" as United Launch Alliance brought the Delta program to a close.

NASA flight engineers managed to photograph and videotape the moon's shadow on Earth about 260 miles below them.

Millions of Americans poured into the solar eclipse’s path of totality to watch in wonder. The excitement was shared across generations for the rare celestial event that saw watch parties across the country as almost all of the continental U.S. saw at least a partial solar eclipse.

A rare total eclipse was visible from Mexico to Canada on Monday, with millions across North America experiencing the celestial phenomenon. "CBS Evening News" anchor and managing editor Norah O'Donnell reports from Indianapolis. Then, CBS News correspondent Janet Shamlian looks at the event's economic impact.

A look back at the esteemed personalities who've left us this year, who'd touched us with their innovation, creativity and humanity.

The Francis Scott Key Bridge in Baltimore collapsed early Tuesday, March 26 after a column was struck by a container ship that reportedly lost power, sending vehicles and people into the Patapsco River.

When Tiffiney Crawford was found dead inside her van, authorities believed she might have taken her own life. But could she shoot herself twice in the head with her non-dominant hand?

We look back at the life and career of the longtime host of "Sunday Morning," and "one of the most enduring and most endearing" people in broadcasting.

Cayley Mandadi's mother and stepfather go to extreme lengths to prove her death was no accident.

The Biden administration is awarding Samsung $6.4 billion to expand American chipmaking. The company will spread the money across at least five facilities in Texas. Sujai Shivakumar, senior fellow at the Center for Strategic and International Studies, joins CBS News to assess the economic and technological impacts.

Israel's military says it will retaliate after Iran and its proxies launched an attack of missiles and drones over the weekend. CBS News foreign correspondent Debora Patta reports. Then, CBS News senior White House correspondent Weijia Jiang explains the U.S.' role in the conflict.

The first criminal trial of a former U.S. president is underway. Jury selection began Monday in Donald Trump's New York "hush money" case. CBS News legal analyst Rikki Klieman joins to discuss.

Jury selection in former President Donald Trump's criminal "hush money" trial began Monday. CBS News chief election and campaign correspondent Robert Costa has more from the courthouse.

Severe thunderstorms, tornadoes and even hail are expected to sweep through parts of the Midwest this week. CBS News national correspondent Dave Malkoff has the details.